FCPA Autumn Review 2018

International Alert

Introduction

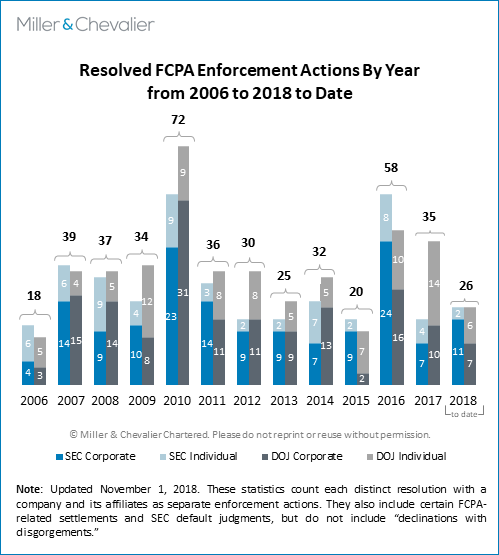

The third quarter of 2018 was a busy time for enforcement of the Foreign Corrupt Practices Act (FCPA), with enforcement actions against six companies, convictions of or settlements with four individuals, and the resolution by the U.S. Department of Justice (DOJ) and Securities and Exchange Commission (SEC) of 10 known investigations without enforcement actions. The quarter also saw a key litigation development in the Second Circuit, potentially narrowing the extraterritorial application of the FCPA.

Three themes stand out from this flurry of activity: First, the SEC had a productive quarter, resolving six enforcement actions and re-emphasizing several of the common challenges that publicly traded companies – "issuers" under the FCPA – may face when seeking to comply with the law's accounting provisions. Second, both the DOJ and SEC continue to wrap up long-running FCPA investigations. Third, the DOJ and SEC continue to resolve a higher-than-average number of FCPA-related investigations without enforcement action, although often without officially "declining" to prosecute pursuant to the November 2017 FCPA Corporate Enforcement Policy. Each of these themes is discussed in greater detail below.

Corporate Enforcement Actions

FCPA corporate enforcement in the third quarter of 2018 was driven by the SEC, which issued a total of six Cease-and-Desist Orders during the period. Much of the conduct covered by these Orders occurred several years ago, in some cases ending in 2012, 2013, or 2014. This suggests that the SEC may be following a trend we have seen over the past year in the DOJ's enforcement of the FCPA – wrapping up long-running, multi-year investigations, potentially freeing up resources for new investigations in the future.

At the same time, all six of this quarter's SEC corporate enforcement actions re-emphasize some of the perennial challenges that FCPA issuers must keep in mind with regard to the law's books-and-records and internal-controls provisions, which require issuers to properly implement accounting controls that, in part, deter foreign bribery. For example, the Stryker Corp. settlement highlights the challenges of ensuring that employees at foreign subsidiaries submit appropriate supporting documentation for transactions and expenses; the Sanofi S.A. and Beam Suntory, Inc. settlements emphasize the importance of ensuring that supporting documentation is in fact legitimate, especially with regard to third party vendors; and the United Technology Corporation (UTC) settlement demonstrates how even well-designed gifts, travel, and entertainment policies and procedures can fail if company personnel fail to follow them. (Each of these settlements and others are summarized below in the Introduction to this FCPA Autumn Review 2018 and discussed in detail in sections on each case.)

The third quarter of 2018 saw activity on the DOJ side as well. Specifically, the DOJ executed two Non-Prosecution Agreements (NPAs), one with the Brazilian national oil company Petróleo Brasileiro S.A. – commonly known as "Petrobras" – and one with Credit Suisse (Hong Kong) Limited, the Hong Kong affiliate of the Swiss investment bank Credit Suisse Group AG. Both NPAs cover conduct that also gave rise to separate Cease-and-Desist Orders from the SEC. The Petrobras settlement is particularly notable as part of the third largest global settlement in anti-corruption history – with a total of $1.7 billion in penalties split between U.S. and Brazilian authorities.

Summaries of this quarter's corporate enforcement actions by the SEC and DOJ are set forth below:

- Beam Suntory, Inc.: On July 2, 2018, the SEC announced a Cease-and-Desist Order for Beam Suntory, Inc. (Beam), a Chicago, Illinois-based producer of several well-known brands of distilled spirits, including the Kentucky bourbons Jim Beam and Maker's Mark, the single-malt Scotches Laphroaig and Auchentoshan, the French cognac Courvoisier, and the Japanese whisky Hibiki. According to the SEC, from 2006 to 2012, employees at Beam's subsidiary in India used fabricated and inflated invoices to reimburse third-party sales promoters and distributors, with the understanding that these illicit payments would be passed on to employees at government-controlled Indian alcohol depots and retail stores to increase sales orders, get better positioning on store shelves, and facilitate distribution of Beam products. Beam India employees recorded these payments as legitimate expenses. Based on this alleged misconduct, the SEC charged Beam with failing to maintain accurate books and records and failing to maintain a sufficient system of internal accounting controls, both in violation of the FCPA. Beam agreed to pay a total of approximately $8 million to resolve these charges. Beam's SEC settlement echoes that of the London-based distilled spirits producer Diageo plc in 2011, which also included alleged misconduct related to inflated commission payments to distributors and sales agents in India. We provide details and analysis of the Beam settlement below.

- Credit Suisse Group AG and Credit Suisse (Hong Kong) Limited: On July 5, 2018, the SEC announced a Cease-and-Desist Order for the Zurich, Switzerland-based investment bank and financial services company Credit Suisse Group AG (CASG). The same day, the DOJ announced an NPA with CASG's Hong Kong subsidiary Credit Suisse (Hong Kong) Limited (CSHK). The charges against CASG and CSHK arose out of CSHK's hiring program in the Asia Pacific region from 2007 to 2013, which allegedly gave preferential treatment to family members of government officials at state-owned entities (SOEs) for employment opportunities or internships, at a time when such SOEs were clients of CSHK. According to the SEC, this hiring practice demonstrated that CASG's internal accounting controls "were insufficiently devised or maintained to reasonably enforce" the bank's policy against such relationship-based hires. According to the DOJ, these "relationship hires" or "referral hires" were part of a quid pro quo with SOE officials to win business. CASG and CHSK agreed to pay a total of $76 million to resolve these FCPA charges. The Swiss investment bank's settlement is similar to the New York-based investment bank JP Morgan's settlement with the DOJ and SEC in 2016 arising out of a similar "Sons and Daughters Program" in the Asia Pacific region. We provide details and analysis of the CASG and CSHK settlements below.

- Sanofi S.A.: On September 4, 2018, the SEC announced a Cease-and-Desist Order for the Paris, France-based pharmaceutical company Sanofi S.A. (Sanofi). From 2011 to 2015, employees and agents at Sanofi subsidiaries in Kazakhstan, the Levant (Jordan, Lebanon, Syria, and Palestine), and the Gulf (Bahrain, Kuwait, Qatar, Yemen, Oman, and the United Arab Emirates) allegedly made improper payments to healthcare professionals in order to be awarded public tenders and increase prescriptions of Sanofi products. According to the SEC, the funds used for these improper payments were generated through fake documentation for purportedly legitimate travel and entertainment expenses, clinical trial and consulting fees, product samples, round table meeting expenses, distributor discounts, and credit notes to distributors – all of which were recorded as legitimate expenses in Sanofi's books and records. Based on this alleged misconduct, the SEC found that Sanofi failed to devise and maintain a sufficient system of internal accounting controls for its subsidiaries in Kazakhstan, the Levant, and the Gulf. Sanofi agreed to pay more than $25 million to resolve charges arising out of the alleged misconduct. Previously, in March 2018, Sanofi had separately disclosed in its SEC filings that the DOJ closed a four-year investigation into the company without criminal enforcement action. We provide details and analysis of the Sanofi settlement below.

- United Technologies Corporation: On September 12, 2018, the SEC announced a Cease-and-Desist Order for the Farmington, Connecticut-based technology conglomerate UTC. The allegations in the SEC Order arise out of a range of alleged misconduct across the company's subsidiaries business units. For example, from 2012 to 2014, UTC's wholly-owned subsidiary Otis Elevator Company (Otis) allegedly executed contracts for the sale of elevator equipment with sham subcontractors and intermediaries with the understanding that the equipment would subsequently be sold to Azerbaijan public housing authorities at inflated prices, thereby creating a pool of money for kickbacks to government officials. Similarly, from 2006 to 2013, UTC's affiliates Pratt & Whitney and International Aero Engines allegedly engaged a sales agent for the sale of airplane engines in China, conducted no due diligence on the sales agent, and agreed to pay him a "success fee commission" of between 1.75 percent to 4 percent of sales to Chinese state-owned airlines, which created a pool of money that could be used for bribes to government officials. Finally, UTC employees reportedly funded leisure travel and entertainment for foreign officials from several countries – including China, Kuwait, South Korea, Pakistan, Thailand, and Indonesia – often by misleading the Legal Department, which was required by company policy to review all such travel. UTC agreed to pay a total of $13.9 million to resolve alleged anti-bribery, books-and-records, and internal-controls FCPA violations. We provide details and analysis of the UTC settlement below.

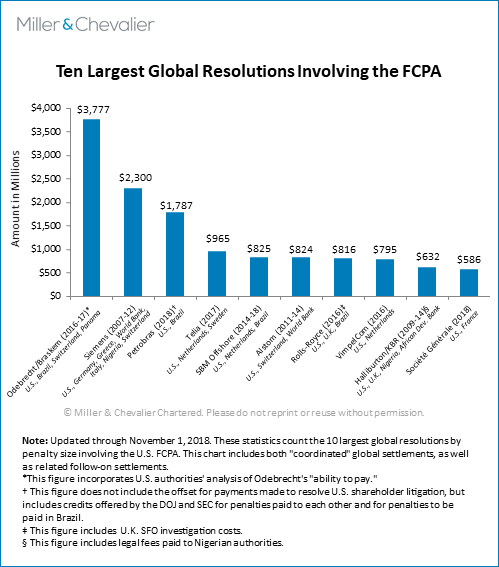

- Petrobras: On September 27, 2018, the Brazilian national oil company Petrobras reached settlements with the DOJ and SEC to resolve FCPA accounting charges arising out of its role at the center of the Operation Car Wash scandal in Brazil. Operation Car Wash has already resulted in several massive global corruption settlements, including the $3.7 billion global Odebrecht/Braskem settlement, the $422 million Keppel Offshore global settlement, a portion of the SBM Offshore $825 million global settlement, and a portion of the $816 million Rolls-Royce global settlement. Petrobras executives allegedly awarded inflated contracts to engineering and oilfield services companies in exchange for bribes that they shared with Brazil's political elite, including two former presidents, dozens of former senators and federal deputies, and other governors, mayors, and cabinet officials. Under the resolutions, Petrobras itself will be held liable for failing to maintain adequate books and records and sufficient internal controls. Altogether, Petrobras will pay up to $1.7 billion to settle U.S. and Brazilian charges. We provide details and analysis of the Petrobras settlements below.

- Stryker Corp.: On September 28, 2018, the SEC announced a Cease-and-Desist Order for Stryker Corp. (Stryker), a Kalamazoo, Michigan-based medical device company. According to the SEC, at the time of the alleged misconduct, Stryker had implemented policies requiring its foreign subsidiaries to properly document transactions; execute written agreements with distributors and sub-distributors that included anti-corruption provisions and audit rights; conduct due diligence on distributors and sub-distributors prior to approval; and provide anti-corruption training to distributors and sub-distributors. However, Stryker allegedly failed to follow these policies in India, China, and Kuwait at various times between 2010 and 2017, resulting in books-and-records and internal-controls violations. For example, Stryker's subsidiary in India allegedly failed to keep and maintain any documentation for up to a quarter of transactions tested in an internal forensic review from 2010 to 2015, during which time certain Stryker India dealers "regularly" issued inflated invoices upon the request of certain private hospitals. Similarly, from 2015 to 2017, several Chinese sub-distributors allegedly did not undergo the due diligence required by company policy, a fact that Chinese employees hid from Stryker management by falsifying certain internal records. Stryker agreed to pay a total of $7.8 million to settle FCPA books-and-records and internal-controls charges. The company previously settled with the SEC in 2014 for FCPA allegations in connection with its business in Mexico, Poland, Romania, Argentina, and Greece. We provide details and analysis of the Stryker settlement below.

Individual Enforcement Actions

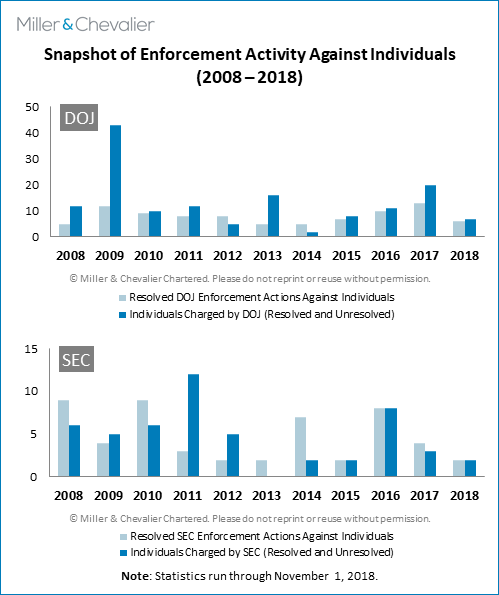

The third quarter of 2018 was also relatively active in terms of individual enforcement actions, with the DOJ and SEC each securing two individual enforcement actions apiece. The DOJ obtained the convictions of Luis Carlos De Leon Perez and Juan Carlos Castillo Rincon, both of whom pled guilty to one count of conspiracy to violate the FCPA anti-bribery provisions for their role in an alleged corruption scheme at Venezuela's state-owned and state-controlled energy company, Petroleos de Venezuela S.A. (PdVSA). The SEC also issued Cease-and-Desist Orders to JooHyun "Dennis" Bahn – who has previously pled guilty for his role in the fraudulent Landmark 72 skyscraper deal described below – and Patricio Contesse González – the former CEO of the Chilean mining company Sociedad Química y Minera de Chile, S.A. (SQM), which reached its FCPA-related settlements of its own with the DOJ and SEC in January 2017.

Despite the third quarter's enforcement actions, 2018 as a whole thus far has lagged in terms of individual enforcement actions, with only four DOJ convictions and two SEC individual enforcement actions all year. Notably, unless the DOJ increases individual enforcement actions in the fourth quarter of the year, 2018 may buck a trend we have seen since 2014 of year-on-year increases of criminal charges against individuals.

The reasons for the 2018 lag in individual enforcement actions and charges is unclear. The previous increase in DOJ individual enforcement actions from 2015 to 2017 likely was attributable to the agency's prioritization of enforcement against responsible individuals – rather than companies – as set forth in the 2015 internal DOJ "Yates Memorandum" and the 2017 FCPA Corporate Enforcement Policy, which conditions a company's declination from prosecution on disclosure of "all relevant facts" about individuals involved in misconduct. The Corporate Enforcement Policy is still in effect, so that emphasis has not changed. Other factors tied to specific cases, some of which may be outside of the DOJ's direct control, could be in play.

Summaries of this quarter's individual enforcement actions by the SEC and DOJ are set forth below:

- Luis Carlos De Leon Perez: On July 16, 2018, former Venezuelan government official Luis Carlos De Leon Perez (De Leon) pled guilty to one count of conspiracy to violate the FCPA and one count of conspiracy to commit money laundering. Specifically, De Leon admitted that he had used his connections as a former government official to solicit and direct bribes and kickbacks from vendors to officials with the Venezuelan state-owned oil company PdVSA between 2011 and 2013 in order to assist the vendors in obtaining PdVSA business, and then conspired with the vendors to launder the proceeds from the bribery scheme. De Leon was arrested in Spain in October 2017 and subsequently extradited to the United States.

- JooHyun "Dennis" Bahn: On September 6, 2018, former New Jersey real estate broker JooHyun "Dennis" Bahn consented to an SEC Cease-and-Desist Order to settle civil books-and-records and internal-controls charges of the FCPA. Bahn's charges arise out of the Landmark 72 corruption scheme, under which Bahn and others at a U.S.-listed global commercial real estate firm allegedly paid $500,000 to a fraudster claiming he would pass a portion of the funds on to a government official from an unnamed Middle Eastern country. Bahn and others allegedly hoped that the payment would induce the unnamed Middle Eastern country's sovereign wealth fund to purchase the Landmark 72 skyscraper in Vietnam, in which Bahn's brokerage firm had a property interest, although the fraudster in actuality had no intention of passing on any funds to any official. Bahn previously pled guilty to criminal FCPA charges arising out of this misconduct, as discussed in our FCPA Spring Review 2018. The civil accounting charges resolved in September 2018 arise out of allegations that Bahn also circumvented the brokerage firm's internal accounting controls, fabricated documents, created fictitious email messages, and lied to company executives, all in furtherance of the $500,000 payment. As part of the settlement with the SEC, Bahn must pay a total of $225,000 in disgorgement. The same day as the SEC Order, Bahn was sentenced to six months in prison for the criminal FCPA charges to which he pled guilty.

- Juan Carlos Castillo Rincon: On September 13, 2018, former U.S. businessman Juan Carlos Castillo Rincon (Castillo) pled guilty to one count of conspiracy to violate the FCPA. From 2011 to 2013, Castillo had served as a manager at a Houston-based logistics and freight forwarding company. During this time, according to Castillo's plea agreement, he conspired with others to bribe a PdVSA official in exchange for assistance in obtaining PdVSA contracts on favorable terms for Castillo's company, as well as inside information about PdVSA's bidding process. Castillo is one of several U.S.-based businessmen who have faced FCPA liability in connection with their work for PdVSA.

- Patricio Contesse González: On September 25, 2018, Patricio Contesse González (Contesse), the former CEO of SQM, consented to an SEC Cease-and-Desist Order to settle civil FCPA charges arising out of his role in causing the Chilean mining company to violate the FCPA, which resulted in settlements with the DOJ and SEC in January 2017. According to the facts alleged by the SEC, from 2008 to 2015, SQM provided discretionary funding to Contesse as CEO for, among other things, travel, publicity, and advisory services. Contesse allegedly used these funds to make payments worth a total of $14.75 million to officials and their relatives from the Chilean government and a Chilean political party, typically through third-party vendors. Based on his role in the scheme, the SEC alleged that Contesse had caused his employer SQM to violate the FCPA's books-and-records and internal-accounting-controls provisions, as well as himself circumventing SQM's internal accounting controls, falsifying SQM's books and records, and misleading the company's accountants. Under the terms of the Order, Contesse must pay a civil penalty of $125,000.

Lastly, the third quarter of 2018 also saw the sentencing of Anthony "Tony" Mace and Robert Zubiate. Both men are former executives at the Dutch offshore oil and gas company SBM Offshore, N.V. (SBM Offshore) and its U.S. subsidiary SBM Offshore USA (SBM USA): Mace previously served as CEO of SBM Offshore and a board member of SBM USA, while Zubiate served as a sales executive at SBM USA. As reported in our FCPA Winter Review 2018, Mace and Zubiate previously pled guilty to FCPA-related charges for their roles in a multi-year scheme to bribe officials at state-owned oil companies Brazil, Angola, and Equatorial Guinea in exchange for assistance in obtaining offshore oil and gas contracts. On September 28, 2018, Mace was sentenced to serve 36 months in prison and ordered to pay a fine of $150,000. The same day, Zubiate was sentenced to serve 30 months in prison and ordered to pay a fine of $50,000.

Investigations Ended Without Enforcement Action

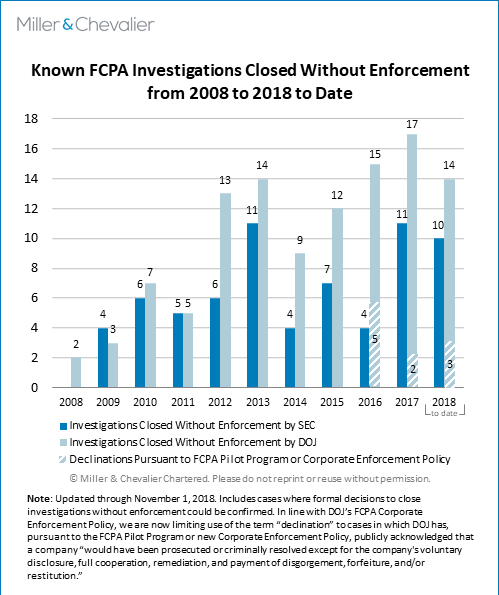

As in past quarters, throughout the third quarter of 2018 Miller & Chevalier has tracked investigations closed without enforcement action, i.e., investigations that the DOJ and SEC have launched but then resolved without a Deferred Prosecution Agreement (DPA), NPA, Cease-and-Desist Order, guilty plea, or other conviction. In July, August, and September of 2018, we tracked ten such investigations closed without enforcement action, including six by the DOJ and four by the SEC – a number significantly above the average over the last ten years, continuing 2018's overall trend in that direction.

Most notably, the third quarter of 2018 saw the second and third official "declinations" under the DOJ's relatively new FCPA Corporate Enforcement Policy. Announced in November 2017, the FCPA Corporate Enforcement Policy offers companies a "presumption" of a declination from prosecution for (1) voluntarily self-disclosing FCPA-related misconduct; (2) fully cooperating with the DOJ in any subsequent investigation; and (3) implementing timely and appropriate remediation. However, the DOJ has thus far only granted declinations under the Policy to three companies: the global intelligence provider Dun & Bradstreet in April 2018, and, this quarter, the Insurance Corporation of Barbados Ltd and Guralp Systems Ltd.:

- Guralp Systems Limited: On August 20, 3018, the DOJ released a letter informing the U.K.-based seismic testing equipment company Guralp Systems Limited (Guralp) that the DOJ had closed an inquiry into possible FCPA and related anti-money laundering violations by the company. According to the DOJ letter, potential FPCA violations may have occurred due to improper payments allegedly made to the director of the Earthquake Research Center at the Korea Institute of Geoscience and Mineral Resources. Nevertheless, based on the FCPA Corporate Enforcement Policy, the DOJ officially declined to prosecute Guralp, noting the company's voluntary self-disclosure, cooperation with the DOJ, and significant remediation efforts, as well as Guralp's cooperation with an ongoing parallel investigation by the U.K. Serious Fraud Office (SFO) allegedly arising out of the same conduct.

- Insurance Corporation of Barbados Ltd: On August 23, 2018, the DOJ released a letter informing the Insurance Corporation of Barbados Ltd (ICBL) that the DOJ had closed its inquiry into possible FCPA violations by the company. Notably, the DOJ letter alleged that ICBL employees and agents had paid approximately $36,000 in bribes to a Barbadian government official in exchange for the government's purchase of two insurance policies. ICBL allegedly collected approximately $686,827.50 in premiums on these policies, earning $93,940 in profits. Despite these allegations, the DOJ officially declined to prosecute the ICBL, noting that the company had satisfied the requirements of the FCPA Corporate Enforcement Policy by voluntarily self-disclosing, cooperating in the DOJ's subsequent investigation, and taking sufficient remediation steps. In addition, the DOJ noted the company's agreement to disgorge the $93,940 in profits from the contracts as issue and "the fact that the [DOJ] has been able to identify and charge the culpable individuals."

Besides the two formal declinations under the FCPA Corporate Enforcement Policy, we tracked eight investigations into six companies by the DOJ and SEC, all officially closed without enforcement action in the third quarter of 2018. These six companies are:

- Hertz Global Holdings: On August 6, 2018, Hertz Global Holdings – the parent company of Estero, Florida-based car rental company The Hertz Corporation – disclosed in a Form 10-Q filed with the SEC that the DOJ and SEC had resolved investigations following the company's self-disclosure of "certain activities in Brazil that raised issues under the Foreign Corrupt Practices Act ('FCPA')."

- Centrais Elétricas Brasileiras S/A: On August 14, 2018, the Rio de Janeiro, Brazil-based electrical utilities company Centrais Elétricas Brasileiras S/A (Eletrobras) disclosed in a Form 6-K filed with the SEC that it had received notice from the DOJ that the agency had elected not to prosecute the company for FCPA-related issues. Although Eletrobras did not clarify the nature of the FCPA-related issues, the company did note that it was continuing to negotiate a related resolution with the SEC.

- Sinovac Biotech Ltd.: On August 20, 2018, the Beijing, China-based vaccine and biopharmaceutical company Sinovac Biotech Ltd. (Sinovac) disclosed in a Form 6-K that the SEC had concluded its investigation into "possible violations of the federal securities laws related to allegations that certain Sinovac employees made improper payments to Chinese government officials," and determined that it would not recommend or pursue an enforcement action. Approximately one month later, on September 17, 2018, Sinovac disclosed in another Form 6-K that the DOJ had similarly closed its investigation into possible FCPA charges without enforcement.

- Ensco plc: On September 4, 2018, the London, U.K.-based offshore drilling contractor Ensco plc (Ensco) disclosed in a Form 8-K that both the DOJ and SEC had informed the company that they had ended investigations into a 2008 drilling services agreement between Pride International LLC (subsequently acquired by Ensco) and Petrobras, the Brazilian national oil company at the center of the Operation Car Wash scandal.

- ING Groep N.V.: On September 5, 2018, Amsterdam, Netherlands-based banking and financial services company ING Groep N.V. (ING) disclosed in a Form 6-K that it had received a formal notification from the SEC that the agency had closed its investigation into alleged misconduct in connection with corruption and money-laundering in Uzbekistan. As discussed in the international developments sections below, ING settled separately with Dutch authorities for their investigation arising out of similar alleged misconduct.

Miller & Chevalier's tracking of such investigations relies on public statements by companies, statements by the DOJ or SEC, or companies' disclosure of such investigations in their securities filings. As such, our tracking is necessarily incomplete, because some companies may elect never to make public either the launch of a DOJ or SEC investigation or its resolution without enforcement action. Nevertheless, tracking investigations closed without enforcement provides a useful data point for assessing the enforcement climate.

Policy and Litigation Developments

In August 2018, the Second Circuit published an opinion in United States v. Hoskins, affirming the dismissal of FCPA charges against a British national and thereby potentially narrowing the jurisdictional scope of the FCPA in certain circumstances. Specifically, the Second Circuit rejected the DOJ's theory that the defendant Hoskins could be held criminally liable for conspiring to violate or aiding and abetting a violation of the FCPA when he could not be held criminally liable for actually violating the FCPA due to his lack of jurisdictional nexus to the United States. It remains to be seen whether other circuits will adopt the interpretation of the FCPA upon which the Second Circuit's opinion relies. Furthermore, the SEC lifted its stay on administrative proceedings following the Supreme Court's decision in Lucia holding the agency's process for appointing Administrative Law Judges (ALJs) unconstitutional. Both the Hoskins opinion and the end of the Lucia stay are discussed in greater detail below.

In addition, on October 11, 2018, Assistant Attorney General for the DOJ Criminal Division Brian Benczkowski announced the publication of a new internal DOJ policy on corporate monitors. We will provide a more detailed analysis of the new DOJ monitor policy in our upcoming FCPA Winter Review 2019. For now, we note that that the new policy appears to formalize many of the DOJ's long-standing practices – most notably the evaluation of the appropriateness of a monitor based on a number of factors, such as the company's corporate compliance program at the time of a resolution, the financial costs of a monitor to the company, and any unnecessary burdens to the company's operations.

International Developments

Lastly, the third quarter of 2018 saw several developments in anti-corruption law outside the United States. The Dutch companies SBM Offshore and ING resolved anti-corruption charges against them in Brazil and the Netherlands, respectively, for their roles in ongoing global corruption scandals. Media in Argentina reported that a former government driver meticulously recorded trips from 2003 to 2015 when he delivered bags of cash to dozens of powerful Argentine government officials from businessmen who had been awarded government contracts. The driver recorded his trips in spiral-bound notebooks – giving rise to the Spanish name for the scandal, i.e., "Los Cuadernos de las Coimas" ("Notebook of Bribes") – which are now at the center of an investigation into dozens of officials, including those close to former Argentinian Presidents Néstor Kirchner and Cristina Fernández de Kirchner.

The Russian Federation amended its Administrative Code to allow leniency for companies that assist officials in uncovering corruption violations – adopting an anti-corruption strategy that many other countries around the world have implemented. Finally, an appellate court in the United Kingdom overturned a previous lower court decision in the ongoing Eurasian Natural Resources Corporation Ltd. litigation, thereby strengthening the U.K. attorney-client privilege as applied to internal investigations.

The ING settlement in the Netherlands, the developing Argentinean bribery scandal, the Russian Federation's new corruption laws, and the U.K. litigation concerning attorney-client privilege are all discussed in greater detail below.

Corporate Enforcement Actions

Beam Suntory Reaches Settlement with the SEC Over Payments by Indian Subsidiary

On July 2, 2018, the SEC announced that Beam Inc., n/k/a/ Beam Suntory, Inc. (Beam), a Chicago-based global maker of spirits and other alcoholic beverages, had agreed to a settlement to resolve allegations that it violated the FCPA's books-and-records and internal-controls provisions. The alleged misconduct centers on the operations of Beam's Indian subsidiary Beam Global Spirits & Wine (India) Private Limited (Beam India) between 2006 and 2012. Beam acquired Beam India in 2006, consolidating Beam India's books and records into its own. At the time, Beam had securities listed on the New York Stock Exchange (NYSE) and was therefore an "issuer" under the FCPA, although it delisted from NYSE after its April 2014 acquisition by Suntory Holdings Limited (Suntory), a Japanese food and beverage conglomerate. As part of the settlement, Beam agreed to pay disgorgement of $5,264,340, prejudgment interest of $917,498, and a civil penalty of $2 million.

According to the SEC's Cease-and-Desist Order (Order), Beam India, with the help of various third parties, made improper payments to a host of Indian government officials to secure product orders, get better placement of its products in government-controlled stores, and obtain required label and license registrations. The SEC alleged that Beam India executives were aware of and directed schemes that involved various third-party distributors, sales promoters, and other affiliates making the payments to officials. The SEC Order details that Beam India generated funds for the improper payments by knowingly paying inflated or false invoices from third parties, with some of the improper payments tracked in off-the-books accounts maintained by Beam India finance executives. According to the SEC, Beam India inaccurately recorded the payments in its books and records, with some then consolidated in Beam's books and records.

India's Alcohol Market

The alcohol market in India is highly regulated, with importation, shipping, manufacturing, warehousing, labeling, and sale to retail stores all subject to government regulations. The Indian alcohol market presents additional regulatory complexity in that each state may have its own laws or regulations relating to various aspects of the industry. During the time period at issue, Beam India sold its products or had warehouses in 26 Indian states and therefore had interactions with a large number of government officials, with its distributors, promoters, bottlers, and other third-party representatives similarly engaged in a significant number of interactions with a wide variety of officials.

Improper Payments

The SEC's allegations of improper payments largely fall into two categories, with both spanning the entire time period from 2006 to the third quarter of 2012. The first category involved Beam India's sale and marketing of products in six markets where both the distribution and retail sale of alcoholic products were subject to government regulation. In these markets, according to the Order, Beam India's third-party promoters directed payments to government officials at retail stores and depots to secure orders and to obtain prominent placement of Beam products in retail stores. The SEC alleged that Beam India's management knew of or authorized the improper payments, and was complicit in generating funds for the payments by accepting for payment promoters' inflated invoices. The Order further claims that some Beam India finance executives maintained a second set of financial records that tracked these payments in some detail. The improper payments were allegedly falsely described in Beam India's books and records as legitimate business expenses, such as customer support, promotional expenses, or distributor commissions, and ultimately consolidated in Beam's general ledger as "Selling and Distribution Expenses."

The second type of improper payments described in the Order concerned improper payments to Indian excise officials. These payments related to inspections of a manufacturing facility, label registrations required for the distribution of Beam products to certain states, and warehouse licenses. One example highlighted by the SEC concerns a label registration for a new product Beam India sought to introduce in 2011. Beam India's third-party bottling facility was unable to obtain label registrations necessary to operate the facility until a meeting with a senior excise official, who sought a payment of one million Rupees or approximately $18,000 to approve the registration. According to the Order, the bottler requested that Beam India fund the improper payment, with Australia-based regional management of Beam India approving the payment and devising a scheme for the bottler to submit false invoices to be reimbursed for the payment. Beam India consequently paid two invoices from the bottler for consulting services approximately equal to the bribe amount.

Inadequate Remediation

The SEC claimed that Beam missed several opportunities to timely remediate the compliance and internal-controls deficiencies underlying the alleged improper payments. The Order notes that Beam engaged a global accounting firm to conduct a compliance review of Beam India in 2010, which found that Beam India's promoters were "likely making grease payments" to government officials and recommended specific follow-up steps, including due diligence to confirm third-party activities on Beam India's behalf. According to the Order, upon a consultation with a U.S. law firm with FCPA expertise, Beam retained an Indian law firm to review and expand the compliance review. The Indian law firm apparently confirmed many of the accounting firm's recommendations, and further noted "that Beam India managers believed that third parties in India may make payments and/or provide gifts to customs officials and government employees" affiliated with the Indian military's Canteen Stores Department (CSD).

The Order notes that around this time, Beam's U.S. law firm informed the company's general counsel's office of SEC's July 2011 FCPA settlement with Beam's direct competitor in the Indian market Diageo plc. The SEC's allegations against Diageo included claims that its subsidiary Diageo India Pvt. Ltd. engaged third-party distributors and sales promoters in India who made illicit payments of approximately $1.7 million to hundreds of Indian officials, including employees of government liquor stores and military canteens, and excise tax and other government administrators, in exchange for increased sales orders, in-store product placement and promotion, label registrations, import permits, and other administrative approvals. According to the Order, the Diageo enforcement action led to a Beam in-house lawyer traveling to India to make further inquiries and conduct additional FCPA training; the lawyer revised Beam India's agreements with certain third parties and used them as templates for other similar agreements.

According to the Order, Beam's U.S. law firm reviewed the work of the Indian firm in August 2011 and found that it lacked an analysis of Beam India's books and records, internal controls or other issues related to its finance and accounting practices, that it did not include sufficient transactional testing, and that it raised issues concerning the conduct and oversight of third parties. The Order highlights Beam's failure to act upon the law firm's recommendation of a financial review, including the engagement of outside forensic specialists, as well as its failure to act upon the accounting firm's earlier recommendation of additional due diligence relating to third parties. Beam allegedly also rejected the Indian law firm's recommendation of interviewing certain local operational employees, apparently out of a concern that the Indian law firm would not assess potential FCPA issues in the same manner as Beam's in-house lawyers would.

The Order further identifies a November 2011 report by a former Beam India employee that a company manager utilized false third-party invoices to generate apparent cash kickbacks, with a subsequent review finding that the cash was in fact used to make payments of $25,000 to government officials in connection with label registration. Despite these findings, Beam did not expand the review to other third parties or other markets in India. According to the Order, a subsequent July 2012 report of similar issues by another former employee led to a broader internal investigation beginning in September 2012, which uncovered the broader corruption schemes involving Beam India management and third parties, including the second set of financial records.

Acknowledgment of Self-disclosure, Cooperation, and Remedial Efforts

In parallel with highlighting Beam's remediation failures before September 2012, the Order acknowledges Beam's voluntary disclosure and its cooperation, such as sharing and summarizing factual findings from its internal investigation, voluntarily producing documents and translating key documents, providing reports on witness interviews, and making current and former employees available to SEC staff. The Order also notes the scope of Beam's remedial actions, which included cessation of business operations at Beam India until Beam was satisfied it could operate Beam India compliantly, terminating certain employees and third parties, enhancing its anti-corruption policies and procedures, including the development and implementation of FCPA compliance procedures related to the issues identified it the investigation, enhancing internal controls and compliance functions, and conducting extensive anti-corruption training throughout the company. In parallel with Beam's self-disclosure to the SEC, the company also disclosed to the DOJ, although the outcome of any resulting DOJ investigation is not yet public.

Noteworthy Aspects

- Relevance of Kokesh and the five-year statute of limitations: After the Supreme Court's June 2017 decision in Kokesh v. SEC, which we discuss in our FCPA Summer Review 2017, SEC's disgorgement claims constitute a "penalty" under federal law and are therefore subject to a five-year statute of limitations under 28 U.S.C. § 2462, the same statute of limitations that applies to the SEC's imposition of civil penalties. The SEC's enforcement action against Beam was initiated, for statute of limitations purposes, on July 2, 2018. The conduct at issue, however, took place from 2006 through 2012, and was therefore entirely outside the five-year limitations period. Given the SEC's imposition of both disgorgement and civil penalty here, the company had probably entered into a tolling agreement with the SEC or waived the limitations period. Given the company's voluntary disclosure to the DOJ and SEC at least as far back as February 2013, Beam's apparent waiver of the limitations issue likely predated the Kokesh decision and was consistent with its cooperative posture. With the new check on the SEC's ability to obtain disgorgement relating to older conduct under Kokesh, companies and individuals currently under the SEC's scrutiny should be more strategic in responding to a potential SEC request for a waiver if any of the conduct at issue falls outside the five-year limitations period.

- Risks in a highly-regulated industry in India: The allegations recited in the Order highlight the risks of working in an Indian industry subject to significant regulatory control and that involves frequent interaction with local regulators. Diageo's settlement with the SEC, noted above, similarly involved allegations that a local subsidiary made payments to government officials through inflated commission payments to third-party distributors who passed on the extra funds to the officials. AB InBev's September 2016 settlement with the SEC likewise involved payments to Indian officials via two third-party sales promoters and a local JV that the company was a partner in, with the local subsidiary funding the payments via inflated commissions and reimbursements and recording the expenses as legitimate promotional costs. The circumstances described in each of these administrative orders provide helpful information for crafting India-specific compliance processes and internal controls, such as a particular emphasis on government inspections, licensing, and permitting, and direct and indirect interactions with the relevant regulators; targeted or more frequent internal audits with a focus on third parties; and deeper due diligence on local third parties and their activities. The involvement or complicity of local employees and management in each of these scenarios likewise suggests that certain business transactions and compliance procedures may require a different level of documentation or approval approach than they might in other jurisdictions.

Credit Suisse Settles with DOJ and SEC Over Improper Hiring Practices in Hong Kong

On July 5, 2018, Credit Suisse (Hong Kong) Limited (CSHK), a wholly-owned subsidiary of financial services company Credit Suisse AG (CSAG), entered into a three-year NPA with the DOJ and agreed to pay $47 million in criminal penalties in relation to its improper hiring practices. On the same day, the SEC issued a Cease-and-Desist Order (SEC Order) against CSAG, in which the company agreed to pay $29.8 million in disgorgement and prejudgment interest for violations of the anti-bribery and internal accounting controls provisions of the FCPA. The total amount of penalties imposed by the two agencies was approximately $76.8 million.

The public documents state that CSAG senior managers in the Asia-Pacific (APAC) area of the company allegedly developed a practice to hire candidates referred from employees of state-owned enterprises (SOEs) and government ministries despite knowing that such hires violated CSAG's compliance policies. From 2007 to 2013, CSAG senior managers in APAC allegedly provided the relatives of government officials and employees of SOEs with internships and paid positions in order to win business from the referral sources. The SEC Order alleges that CSAG ultimately derived over $46 million in revenue from the Chinese SOEs whose executives referred candidates hired by CSAG or over which government officials who referred candidates had influence.

According to the SEC Order and the NPA, during the relevant timeframe, CSAG had in place an anti-bribery policy that prohibited "employment, including internships, to Government Officials, their family members, or associates" if offered in order to obtain or retain business. The policy's definition of "Government Officials" included SOE personnel. The SEC Order describes the CSAG's Legal and Compliance Department (LCD) advising managers in APAC not to hire candidates in APAC and Hong Kong referred by SOE clients, determining that such hires could violate the FCPA and were "too great a risk." Despite LCD's advice, senior CSHK managers and CSAG managers in APAC allegedly took steps to onboard referral hires outside of the company's established recruiting program. CSAG managers in APAC allegedly instructed subordinates to take measures to give the appearance that they were following the normal hiring process, including drafting resumes for a referral hire or artificially inflating ratings on hiring forms.

According to the SEC Order, correspondence between senior CSAG managers in APAC highlighted the potential business deals that candidates could bring and their close relationships with senior management at SOEs. According to the NPA, one employee explained, "relationship hires have to translate to $" or "the relationship is worthless to our organization." CSAG allegedly maintained spreadsheets of referral hires that included information identifying the referring client or relationship with regulators. Some spreadsheets allegedly identified specific deals that could come from the relevant hire.

According to the NPA, CSAG referral hires were less qualified, had less relevant experience, and lacked technical skills in comparison with candidates hired through CSAG's normal employment channels. In fact, CSAG bankers in the U.S. allegedly complained about the poor quality of referral hires, with one senior banker writing "we have had really bad experiences with many of the individuals from Asia . . . [a particular Credit Suisse HK senior manager] generates most of them and there is enough frustration in the system over this at this point that I wanted to check in with you for a sanity check on whether we should always break the mold for his requests or not . . . ." Despite the frustration and poor performance of the referral hires, the case documents note that CSAG continued to provide promotions and benefits to referral hires throughout the course of their employment at the request of SOE or government officials.

According to the NPA, CSAG earned over $46 million in revenues from transactions brought to the bank by the SOE executives who were connected to the referral hires. The DOJ applied an aggregate discount of 15 percent off the bottom of the U.S. Sentencing Guidelines fine range based on the reduced credit that CSAG and CSHK received for cooperation and remediation. CSAG and CSHK did not receive voluntary disclosure credit because neither entity voluntarily or timely disclosed the conduct to the DOJ. The NPA states that CSAG and CSHK received partial credit for their cooperation with the investigation by performing an internal investigation, making factual presentations to the DOJ, producing documents and translations, making employees in foreign countries available for interviews, and disclosing all relevant facts on the misconduct. However, the NPA states that "the Company did not receive full cooperation credit because its cooperation was reactive, instead of proactive." CSAG and CSHK likewise did not receive full credit for remediation, despite implementing additional policies and procedures designed to prevent the type of improper hiring at issue, "because [they] did not sufficiently discipline employees who engaged in the misconduct, and instead only recorded policy infractions internally and provided notices of infractions to three employees."

Despite the lack of full cooperation or remediation credit, the DOJ determined that CSAG and CSHK did not need an independent compliance monitor based on the state of their compliance programs and their agreement to self-report to the DOJ. The NPA obligates CSAG and CSHK to report the status of its remediation and implementation of compliance measures to the DOJ at twelve-month intervals during the three-year period. During this period, CSAG and CSHK must conduct an initial review and submit an initial report of its anti-corruption remediation efforts and propose designs to improve compliance internal controls, policies, and procedures. CSAG and CSHK must undertake at least two follow-up reviews incorporating the DOJ's views on prior reports to assess whether their policies and procedures are reasonably designed to detect and prevent violations of the FCPA. The SEC Order did not impose ongoing reporting requirements.

Noteworthy Aspects

- Employment as an Improper Benefit: CSAG is the fourth company to enter an FCPA settlement based primarily on improperly hiring individuals related to foreign government officials in exchange for business deals. Other FCPA settlements involving the hiring of individuals, usually family members, referred by SOE or government officials in order to secure business include BNY Mellon, Qualcomm, and JP Morgan. All but one of the settlements – BNY Mellon– have been based on activities in China. The CSAG settlement emphasizes the particular bribery risks presented by hiring practices in China. Given the heavy emphasis on relationships, or guanxi, improper requests for employment may occur more frequently in China than in other countries. Companies should ensure that they have the appropriate safeguards to prevent such hires and monitor the effectiveness of such controls.

- Lack of Compliance Monitor: The DOJ's decision not to impose a monitor on CSAG or CSHK appears to be consistent with recent statements by the Assistant Attorney General for the Criminal Division at DOJ, Brian Benkczowski, that the DOJ has revised its guidelines on the imposition of corporate monitors. According to Benkczowski's remarks, when determining whether a monitor is needed, the DOJ must consider the type of misconduct, the pervasiveness of the conduct, whether it involved senior management, and any improvements a company has made to its corporate compliance program. The decision not to impose a monitor in CSAG and CSHK is noteworthy because the NPA alleges that the company failed to cooperate or remediate "proactively" over the course of the investigation, the alleged misconduct occurred over a period of six years, and the alleged misconduct involved active circumvention of the company's existing compliance controls. The CSAG settlement may offer insight as to whether companies should expect the imposition of a monitor under similar circumstances.

- Partial Remediation Credit: The DOJ's decision not to give CSAG and CSHK full credit for remediation was also consistent with the DOJ's 2017 Evaluation of Corporate Compliance Programs guidance that companies must adequately discipline wrongdoers in order to receive full remediation credit. Despite implementing numerous remedial measures, including: additional controls related to their hiring programs; procedures to ensure the identification of and anti-corruption vetting for all candidates referred for employment by government officials and employees of SOEs; screening by an independent service for connections to government officials, SOE employees and other "politically exposed persons" (PEPs) and verifying the efficacy of this screening; post-hire controls on employees linked to government officials and SOE employees; and yearly headcount reviews to ensure accurate record-keeping concerning hiring, among others. According to the NPA, the company did not receive full remediation credit "because it did not sufficiently discipline employees who engaged in the misconduct, and instead only recorded policy infractions internally and provided notices of infractions to three employees." The CSAG and CSHK settlement is notable because it signals that the DOJ expects strong disciplinary responses such as termination.

Sanofi Settles with SEC Over FCPA Allegations in Kazakhstan and the Middle East

On September 4, 2018, French pharmaceutical giant Sanofi S.A. (Sanofi), which trades American Depositary Receipts (ADRs) on the NYSE, agreed to pay more than $25.2 million in penalties to resolve charges that the company had violated the books-and-records and internal-controls provisions of the FCPA as a result of alleged bribery-related activities by several of its subsidiaries. According to the SEC's Cease-and-Desist Order, the company's Kazakhstan and Middle East subsidiaries engaged in a variety of schemes to make corrupt payments to government healthcare professionals (HCPs) and procurement officials to secure tenders to increase the prescription of its products.

According to the SEC Order, between 2007 and 2011, Sanofi-Aventis Kazakhstan LLP (Sanofi KZ) allegedly used distributors as part of a kickback scheme to generate funds with which to bribe Kazakh officials to ensure the company was awarded tenders with public institutions in the country. The scheme, which reportedly produced more than $11.5 million in illicit profits, operated as follows: (1) senior managers at Sanofi KZ would flag certain public tenders for its distributors, who would then submit bids; (2) once a tender was awarded, Sanofi KZ would provide the distributor with an excessive discount or credit note (agreed upon in advance) on the sales price between the distributor and the public institution (generally between 20-30 percent); (3) the distributor would then kick back a designated portion of the funds generated by the discount to certain Sanofi KZ employees, who would deliver them to the Kazakh official(s) involved in awarding the tender. The kickbacks to Sanofi KZ employees were tracked using internal spreadsheets and referred to internally as "marzipans."

Between 2011 and 2013, employees at Sanofi-Aventis Liban S.A.L. (Sanofi Levant), the company's Lebanon-based subsidiary, allegedly participated in a series of schemes to convey benefits to HCPs through "sponsorships, gifts, donations, product samples, consulting agreements, peer-to-peer meetings, clinical studies, and grants" and reportedly produced more than $4.2 million in illicit gains. These schemes were executed across the various business lines, included the top selling products of Sanofi in the region, and sometimes involved participation by Sanofi Levant senior managers.

The SEC stated that the improper conduct at Sanofi Levant "w[as] not isolated and spanned across government agencies as well as private institutions." For example, notwithstanding a policy requirement that product samples have a medical justification, sales representatives at Sanofi Levant donated 24 vials of Taxotere, one of the company's most expensive products, to a large, public hospital in Jordan "as a favor" to a key opinion leader (and tender committee member) at the hospital, without consideration of the purpose of the donation or its appropriateness and with an oncology manager rather than Medical Affairs reviewing and approving the request. Sanofi Levant also paid this key opinion leader significant amounts in questionable fees over a period of years, which were paid by check to an unrelated individual, including: the equivalent of $28,900 in consulting fees for hosting events and training HCPs in Iraq (services for which there is no supporting documentation), $25,997 in clinical trial fees (although no reports on trial findings or observations have ever been provided), and $5,500 in speaking fees. The subsidiary also engaged other influential HCPs in the region as consultants, who provided the company with vague services for which there is little to no documented support, including a private sector pharmacist in Lebanon who was paid $237,000 over the course of five years for consulting services that it is unclear were ever provided.

Finally, until 2015, sales representatives at Sanofi Aventis Gulf FZE (Sanofi Gulf), the company's UAE-based subsidiary, allegedly carried out a long-standing scheme under the direction of their managers "to submit false travel and entertainment reimbursement claims, pool the illicit proceeds of the false schemes, and distribute the illicit proceeds to HCPs in the private sector in order to increase prescriptions of Sanofi products." These reimbursement claims, which reportedly generated more than $1,751,567 in illicit profits, involved round-table meetings that did not occur and were enabled by fake receipts issued by collusive vendors known to facilitate such activity. One Sanofi Gulf employee estimated that 70 percent of the travel and entertainment expenses submitted by one business unit during the relevant period were related to the scheme.

Under the terms of its settlement, Sanofi consented to the entry of a Cease-and-Desist Order and agreed to pay $5 million in civil penalties, $17,531,666 million in disgorgement, and $2,674,479 million in prejudgment interest, as well as to self-report periodically to the SEC on the status of its remediation and compliance program over the next two years.

Noteworthy Aspects

- Sanofi's Voluntary Self-Disclosure: Sanofi initiated an internal investigation in mid-2014 upon receiving a series of anonymous allegations about wrongdoing that reportedly occurred between 2007 and 2012 in parts of the Middle East and East Africa. The company also self-disclosed the allegations to U.S. authorities and cooperated with the DOJ and SEC in the subsequent investigation, which allegedly identified misconduct as recent as 2015.

- Underlying Allegations Beyond the Stated Statute of Limitations: Some of the Sanofi allegations date back to 2007—approximately 11 years ago. While conduct between 2007 and August 2013 would typically fall outside of the statute of limitations following last year's Kokesh decision, it is likely that Sanofi, in cooperating with U.S. authorities, agreed to toll the statute.

- Agencies Did Not Bring Anti-Bribery Charges: Although the SEC Order explicitly describes reported bribery by several Sanofi subsidiaries, neither the SEC nor the DOJ, which in February closed its parallel inquiry into the allegations without enforcement, charged Sanofi with violating the FCPA's anti-bribery provisions. The lack of anti-bribery charges suggests that the agencies might have had difficulty meeting the intent or jurisdictional elements required for such charges. For instance, the SEC Order does not allege any knowledge by Sanofi (the parent issuer) in the underlying misconduct nor does it describe any involvement by U.S. persons or entities or the use of any means or instrumentality of interstate commerce. Sanofi's public disclosures provide limited insight into the DOJ's justification for closing its inquiry without enforcement, but they do indicate that the company cooperated with the agency in its investigation. Notwithstanding the lack of anti-bribery charges, the SEC still required Sanofi to disgorge over $17 million in allegedly illicit profits linked to its accounting provision violations.

- Insight into the SEC's Compliance Expectations: The SEC Order highlights several alleged internal control failures that provide insight into the SEC's compliance expectations, such as:

- Standardizing distributor discounts: The Order implies that companies ought to have controls in place to standardize and monitor discounts, noting that: "At the time, Sanofi had no standardized commercial policy for distributor discounts and did not review the discounts provided by local management."

- Monitoring of outsourced distributor promotional activities: The Order cites an internal company audit that identified a lack of monitoring of outsourced distributor promotional activities (including distributor-organized roundtables) that auditors said were not in compliance with Sanofi policy.

- Conducting periodic audits of affiliate internal accounting controls: Finally, the Order notes that Sanofi had not conducted a full audit of Sanofi Gulf's commercial operations in eight years, highlighting the expectation that a company conduct periodic audits of its higher-risk operations.

- Description of Sanofi's Extensive Cooperation and Remediation: The SEC cited extensive cooperation by Sanofi, including that the company "provided regular briefings regarding the facts developed in its internal investigation" and "timely conveyed the facts it learned in the course of its investigation, including facts that the Commission would not have been able to readily and independently discover, produced and highlighted particularly relevant documents, promptly responded to additional requests by the Commission staff, and provided translations of documents as needed." The SEC also noted that prior to the Commission's investigation, Sanofi had begun independently enhancing its compliance program by, among other things, developing a centralized program, revamping its internal controls and procedures over HCP expenditures, increasing the number of its compliance officers globally, enhancing the operation of local compliance committees, and placing compliance personnel in high-risk local markets. The company also enhanced its relevant policies and procedures, including those dealing with training, audits, third-party due diligence, and event monitoring. Finally, the company reportedly terminated 121 employees, including senior local business managers, accepted resignations from another 14 employees, and disciplined 49 employees.

- Context within Broader Enforcement Landscape: While Sanofi's resolution represents the first FCPA enforcement action involving a pharmaceutical company since December 2016 (Teva Pharmaceuticals), agency scrutiny of the life sciences industry has nevertheless been constant. During that same time period, the DOJ and SEC have brought enforcement actions against three medical device manufacturers, and they currently have open investigations involving upwards of a dozen pharmaceutical and medical device companies. The enforcement landscape, however, does appear to have shifted somewhat in the wake of the FCPA Corporate Enforcement Policy announced last year, with the agencies opting to close or decline cases against an increasing number of companies, including several companies in the life sciences sector. This uptick in closures and declinations could be attributable to, among other things, benefits accorded in recognition of the companies' notable compliance and cooperation, an effort to avoid "piling on," and a less aggressive posture in borderline cases where it is arguable whether the elements of a violation have been met.

United Technologies Corporation Settles FCPA Claims with SEC for $13.9 Million

On September 12, 2018, the SEC announced that United Technologies Corporation (UTC) reached a settlement to resolve charges that it violated the anti-bribery, books-and-records, and internal-accounting-controls provisions of the FCPA by making unlawful payments to government officials. UTC agreed to pay $13.9 million to the SEC, consisting of disgorgement of $9,067,142 plus interest of $919,392 and a penalty of $4 million. UTC in part designs, manufactures, and markets high-technology products and services to building and aerospace industries. The company is headquartered in Connecticut, incorporated in Delaware, and trades on the NYSE, making it a domestic concern and issuer under the FCPA.

According to the SEC Cease-and-Desist Order, UTC's wholly-owned subsidiary Otis Elevator Co. (Otis) made unlawful payments to officials in Azerbaijan to facilitate the sales of elevator equipment and as part of a kickback scheme to sell elevators in China. From 2012 to 2014, Otis engaged in various schemes to sell its elevator equipment to Baku Liftremont, a municipal entity responsible for procuring and maintaining the elevators in public housing in Baku. The SEC Order states that the schemes involved the use of sham subcontractors and intermediaries to make improper payments to officials of Baku Liftremont.

One scheme, for example, involved a direct sale from Otis's branch based in Russia (Otis Russia) to Baku Liftremont of elevator equipment valued at $1.8 million, which was facilitated through two subcontractors. According to the SEC, no due diligence was performed on the subcontractors or the contracts, and they were paid nearly 44 percent of the contract value. Additionally, between February 2013 and December 2014, at the direction of a Liftremont senior official, Otis Russia involved four different intermediaries that made improper payments to secure nine contracts from Liftremont. Otis Russia sold elevator equipment to the intermediary at one price but knew that the intermediary would sell the equipment to Liftremont at a higher price; the spread between the prices was intended for Liftremont officials. No due diligence was performed on the intermediaries. Otis Russia prepared customs paperwork to facilitate transportation of the equipment across borders and into Azerbaijan. In total, between March 2012 and August 2014, Otis Russia entered into ten contracts worth $14.6 million to sell elevator equipment to Liftremont. The SEC noted that, separately, in 2012, Otis's China branch also made payments as part of a kickback scheme to sell elevators in China.

In addition, the SEC Order found that from 2009 to 2013, UTC, through International Aero Engines (IAE), a joint venture of a division of UTC, Pratt & Whitney, made payments to a Chinese sales agent with no background or expertise in the airline industry to increase IAE's market share in China. IAE and Pratt & Whitney conducted minimal due diligence on the sales agent and "disregard[ed] the high probability that at least some of the money would be used to make unlawful payments to a Chinese official." In 2009, for example, IAE competed for a contract with a Chinese state-owned airline. The sales agent assisted IAE with the campaign for the contract and requested a commission advance of $2 million purportedly for an office expansion. The agent provided no documentation to support this. The following month, a Chinese airline official emailed the agent confidential information about the tender, which the agent provided to the General Manager and Vice President of Customer Business at IAE. IAE modified its bid in response, and IAE won the contract. The SEC Order states that, between March and December 2009, the agent made at least six payments totaling over $160,000 to the airline official who provided the confidential document.

Finally, from 2009 to 2015, the SEC determined that UTC improperly provided trips and gifts to various foreign officials from China, Kuwait, South Korea, Pakistan, Thailand, and Indonesia through its Pratt & Whitney division and Otis to obtain business worth $9 million. Between 2009 and 2015, UTC improperly recorded over $134,000 in illegitimate travel and entertainment for foreign officials in the company's books and records as legitimate business expenses.

UTC self-reported the misconduct and cooperated with the SEC's investigation. The SEC Order also notes that UTC terminated employees and third parties responsible for the misconduct, enhanced its internal accounting controls, and enhanced the applicable due diligence processes. UTC consented to the SEC Order without admitting or denying any violations of law.

Noteworthy Aspects

- Ineffective Oversight: The SEC Order emphasized that transactions did not follow normal procedures and that Legal, Finance, and business employees all failed to prevent improper transactions. In particular, the SEC Order noted that, in reviewing contracts for anti-corruption purposes, Legal personnel "merely confirmed that the contained standard terms" without "[seeking] to confirm that the intermediaries had undergone due diligence as required by Otis policies or inquired about contractual terms that showed that the intermediaries were acting as distributors." Similarly, the SEC Order noted that Legal, Finance, and business employees approved using Liftremont as a distributor for government-facing elevator projects "despite numerous red flags, including the fact that Liftremont was the government entity responsible for the selection of the supplier for Baku municipal and government projects." In fact, one in-house Otis lawyer in Russia initially refused to approve the insertion of a new intermediary into Liftremont's contract, requesting additional information on the intermediary's ownership and business justification. However, the in-house lawyer eventually signed off on the contract after his superior presented him with a perfunctory explanation for the new intermediary. The SEC Order illustrates the need for parent companies to monitor subsidiaries and question behavior that raises red flags.

- Ineffective Gifts, Travel, and Entertainment Program: The SEC Order also noted that company personnel failed to follow UTC policies for the review of leisure travel and entertainment for foreign officials. For example, the Order notes that the company's Legal Department was required to review and approve all leisure travel and entertainment plans to foreign officials. However, company personnel circumvented this requirement by (1) submitting travel for foreign officials without disclosing the leisure travel/entertainment component or (2) including the travel as a cost component in contracts with the government end customer – such as the South Korean air force – which were not subject to the same level of leisure travel/entertainment review. The Order further states that, even when Legal personnel did review travel expenses related to foreign officials, they often failed to note basic red flags indicating leisure travel/entertainment, such as travel to tourist destinations such as Orlando, Florida, where the company did not have facilities. Like many past FCPA settlements, the UTC settlement reiterates the risk of "paper" gifts, travel, and entertainment programs, which may be sufficient on paper but are not properly followed or adequately enforced.

Petrobras Resolves Books-and-Records, Internal-Controls, and Related Charges with the DOJ, SEC in Connection with Illegal Payments to Petrobras Officials, Politicians, and Political Parties in Brazil

On September 27, 2018, the DOJ and SEC announced that they had reached agreements with Petrobras to resolve books-and-records, internal-controls, and related charges in connection with illegal payments to Petrobras officials, many of which were passed on to politicians and political parties in Brazil. According to a company statement made the same day, the settlement with U.S. authorities was coordinated with a pending settlement between Petrobras and the Ministério Público Federal (MPF) in Brazil.

Petrobras is a state-owned Brazilian energy company, incorporated and headquartered in Brazil and operating in 18 other countries including the United States. The company's shares are publicly traded in the United States, making the company an "issuer" under the FCPA.

The NPA with the DOJ

According to the NPA with the DOJ, between at least 2004 and 2012, Petrobras's executives participated in corruption schemes by receiving bribes, as well as facilitating and directing millions, if not billions, of dollars to other Brazilian politicians and political parties. According to the NPA, Petrobras executives participated in a "massive bid-rigging scheme," which allowed contractors to obtain contracts from Petrobras through non-competitive means. Typically, the contractors paid bribes totaling between one to three percent of the value of the contracts improperly obtained from Petrobras. The bribe payments were often disguised as fictitious expenses included in consultancy agreements and were shared among Petrobras executives, Brazilian politicians, Brazilian political parties, and various intermediaries who helped to facilitate the payments. In return, Petrobras "remain[ed] in the favor of many of Brazil's politicians and political parties." In addition, the NPA notes that some of the corrupt payments paid to Brazilian politicians and political parties "could affect" Petrobras, including because the respective politicians and political parties receiving bribes had oversight over locations where Petrobras was carrying out projects.

The NPA summarizes various examples of the corrupt schemes, including the millions of dollars in bribes paid in connection with the Abreu e Lima Refinery in the Brazilian state of Pernambuco, the Rio de Janeiro State Petrochemical Complex, and large contracts with ship operating, shipyard, and drillship companies. According to the NPA, although the total amount of bribes paid is unknown, "more than U.S. $2 billion has been estimated to have been generated and used to make corrupt payments, more than approximately U.S. $1 billion of which was estimated to have been directed to politicians and political parties."

Petrobras admitted to violating the FCPA's books-and-records and internal-controls provisions pursuant to 15 U.S.C. §§ 78m. Specifically, the NPA stated that, as a result of the corrupt schemes, Petrobras "failed to make and keep books, records, and accounts which accurately and fairly reflected the Company's capitalization of property, plant, and equipment ("PP&E"), which was overstated on the Form 20-F as a result of the bribes being generated by the Company's contractors with the cooperation of certain Petrobras executives." In addition, three executives involved in the corrupt scheme signed Sarbanes-Oxley (SOX) 302 sub-certifications, which required the executives to certify that the Form 20-F filed with SEC did not contain materially false or misleading statements. The NPA further states that the CFO of a Petrobras subsidiary, also involved in the corrupt schemes, signed a management representation letter provided to external auditors, certifying that he was unaware of fraud affecting the subsidiary that would significantly affect its financial statements.

In addition, according to the NPA, Petrobras executives knowingly and willfully failed to implement internal financial and accounting controls to continue the facilitation of bribes to Brazilian politicians and Brazilian political parties, including a failure to implement internal controls over the contracting process for services relating to large investment projects. Specifically, internal controls deficiencies highlighted in the NPA include: "failure to implement appropriate due diligence procedures for the retention of third-party vendors; failure to implement sufficient oversight to prevent the revision of estimates at the conclusion of the bid phase to favor certain bidders; failure to implement sufficient safeguards to prevent the manipulation of bid participant lists or criteria for selecting bid invitees to permit the invitation of companies that were not qualified; failure to implement a selection process that would prevent projects from being improperly awarded through direct contracting instead of a tender process; and manipulation of bid evaluation criteria to favor bribe-paying companies."

SEC Administrative Order

The SEC Order notes from at least 2004 to April 2012, during a time when Petrobras was carrying-out a large-scale expansion of its infrastructure, various "Corrupt Executives" at Petrobras worked with a "cartel" of Petrobras contractors and suppliers to rig bids and subsequently inflate the costs of Petrobras's projects by billions of dollars. In exchange, the contractors paid kickbacks (typically between one to three percent of the total contract value) to Corrupt Executives, politicians and political parties, including the same Brazilian politicians who gave the Corrupt Executives their jobs at Petrobras. In addition, the Order states that from 2003 to 2012, Corrupt Executives engaged in other bribery schemes with companies that wanted to win contracts or receive more favorable contract terms. In one instance, at the recommendation of an executive who received a $2.5 million bribe payment, Petrobras purchased a Texas oil refinery despite the executive knowing that the structure was inadequate for the company's needs and would require a "massive" amount of capital to fix. Part of the $2.5 million bribe payment was passed onto a Brazilian politician.

As a result of the corrupt schemes, the Order states that Petrobras violated the books-and-records and internal-accounting provisions of the FCPA. In addition, the company violated Sections 17(a)(2) and (3) of the Securities Act (prohibiting the offer or sale of any security through false statements of a material fact, omission, fraud, or deceit) and Section 13(a) of the Exchange Act (requiring every issuer of a security registered pursuant to Section 12 of the Exchange Act to file annual reports that do not contain misleading statements).

With regards to the books-and-records violations, the corrupt schemes caused Petrobras to report inflated assets in its Financial Statements filed with the SEC, such as its Form 20-F for fiscal years 2009 through 2013 (including materials incorporated by reference in Petrobras's 2010 $10 billion public offering documents). In addition, the filings contained various misstatements and omissions about the integrity and quality of Petrobras management, as well as its relationship with the Brazilian government and its suppliers and contractors.

With regards to the internal-controls violations, the Order noted that Petrobras did not require employees to receive anti-corruption, anti-fraud, or compliance training, lacked policies addressing interactions with government officials, had "deficient" procurement policies and procedures, did not have a "typical" compliance function until 2014 despite requirements included in its Audit Committee Charter, and had no formal vetting process for appointing senior executives.

Penalties and Offsets

Excluding the offsets and credits discussed herein, Petrobras agreed to pay $1.787 billion in total penalties and disgorgement to U.S. and Brazilian authorities. According to the DOJ NPA, Petrobras agreed to pay a total criminal penalty of $853.2 million which includes a 25 percent discount for full cooperation and remediation pursuant to the U.S. Sentencing Guidelines. The DOJ determined that an independent compliance monitor was unnecessary. However, the company is required to self-report to the DOJ "at no less than twelve-month intervals" for three years regarding its remediation efforts and the implementation of its compliance program and internal controls.

The SEC Administrative Order required the company to pay a penalty in the amount of $853.2 million "to the Commission in connection with [its] Order and as described in the [NPA] with the [DOJ]" and $933.5 million in disgorgement and prejudgment interest.