FCPA Autumn Review 2016

International Alert

Introduction

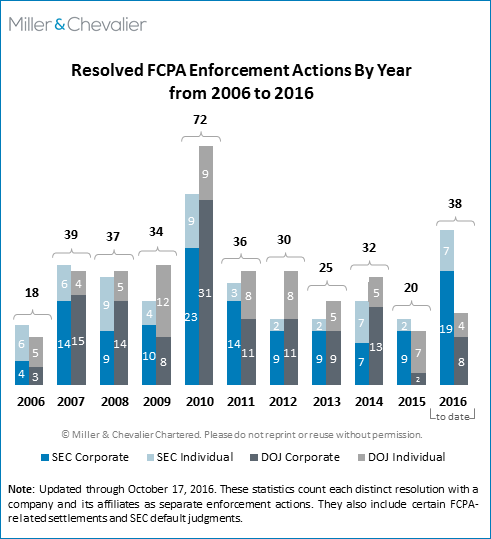

Enforcement activity under the U.S. Foreign Corrupt Practices Act (FCPA) remained high during the third quarter of 2016, with U.S. authorities entering into 14 new FCPA-related dispositions, including 11 by the U.S. Securities and Exchange Commission (SEC or Commission) and three by the U.S. Department of Justice (DOJ or Department). Together, the SEC and DOJ have resolved 38 enforcement actions through September of this year, already exceeding their combined annual totals for every year since 2010. If this brisk pace is maintained through the end of the year, the agencies will end 2016 with at least 48 enforcement actions, the second-highest annual total in the FCPA's history.

The SEC's and DOJ's FCPA-related activity over the past quarter highlights the interplay between the agencies' respective approaches to enforcing the statute. Some recurring patterns, which we have touched on in past FCPA Reviews and explore further below, include:

- the SEC pursuing and resolving more corporate enforcement actions as the DOJ shifts its focus toward larger cases involving more serious misconduct;

- an increase in publicly reported DOJ declinations (i.e., formal decisions to close an investigation without bringing an enforcement action); and

- the DOJ's implementation of its new FCPA pilot program, which, beyond serving as another avenue to promote the reported benefits of self-disclosure and cooperation, is also the vehicle that introduced the latest tool in the DOJ's enforcement toolbox: a declination that requires the disgorgement of alleged ill-gotten gains, as compared to typical declinations, which involve no payment of any type.

Resolved Enforcement Actions

The SEC resolved eight corporate and three individual FCPA enforcement actions this quarter, for a total of 26 dispositions for the year. The DOJ resolved three corporate FCPA enforcement actions over the same period of time, bringing the Department's disposition total to 12 through the end of September. As the chart below demonstrates, the SEC has continued to ramp up its FCPA-related enforcement efforts, with its 11 dispositions this quarter constituting almost half of its FCPA activity in 2016 to date and nearly matching its year-end totals in each of the last four years. The Commission's 26 resolved enforcement actions so far this year exceed its total number of FCPA dispositions from any prior year except for 32 in 2010 and, at this rate, will likely match or exceed that total by year's end. By contrast, the DOJ's FCPA-related enforcement activity this year has been flat, generally consistent with the Department's pace over the past several years, with the exception of an anomalous 2015, the reasons for which we analyzed in our FCPA Winter Review 2016.

Reflecting the geographic trends in FCPA enforcement that we discussed in our FCPA Summer Review 2016, a disproportionate number of this quarter's resolved enforcement actions continue to relate to activities in China, with the rest set in Latin America, Africa, Russia, and India. The corporate and individual settlements this quarter run the gamut in terms of industries involved, types of misconduct alleged, and scope of the reported violations.

Four of the SEC's eight corporate FCPA dispositions this quarter involved alleged misconduct in China and required defendants to pay monetary assessments ranging from $765,688 to $20 million stemming from the conduct of their Chinese subsidiaries. Two of these enforcement actions - settlements with U.K.-based AstraZeneca plc (AstraZeneca) and GlaxoSmithKline plc (Glaxo) in August and September, respectively - highlight the SEC's continued focus on the healthcare industry, as discussed in our FCPA Spring Review 2016, and the particular emphasis on healthcare companies operating in China, explored in the Novartis case section of that Review. In its enforcement actions against both AstraZeneca and Glaxo, the SEC alleged that employees of their foreign subsidiaries falsified expenses, directly and by colluding with certain third-party vendors, to generate the funds necessary to make improper payments to government-employed health care providers (HCPs) in China (AstraZeneca and Glaxo) and Russia (AstraZeneca). The other two enforcement actions - the July settlement with Utah-based multi-level marketer Nu Skin Enterprises, Inc. (Nu Skin) and the September settlement with Wisconsin-based provider of building efficiency systems and specialty automotive products Johnson Controls, Inc. (Johnson Controls) - further underscore the broad nature of the risks associated with operating China. The Johnson Controls case involved a Chinese subsidiary that was implicated in another FCPA disposition in 2007, shortly after being acquired by Johnson Controls. In response to the company's efforts to remediate certain internal-controls weaknesses identified in the wake of that disposition, employees at the Chinese subsidiary reportedly devised another scheme to circumvent the new controls. The Nu Skin case centered on an allegedly improper charitable contribution - a rare sole basis for an FCPA enforcement action. According to the SEC, the company's Chinese subsidiary made a large payment to a charity established by a high-ranking Chinese party official in exchange for his assistance in an ongoing provincial investigation into the subsidiary's potential noncompliance with local law.

The other corporate FCPA enforcement actions brought by the SEC are more varied in their geographical scope. In July, the SEC reached a $9.4 million FCPA settlement with Chile-based LAN Airlines S.A. (LAN) as part of a $22.2 million joint resolution by LAN and its parent company LATAM Airlines Group S.A. (LATAM) with the SEC and the DOJ. These parallel actions related to alleged payments made in connection with a union dispute in Argentina and turned on the same facts that led to a settlement by LAN's CEO with the SEC in February of this year (see our FCPA Spring Review 2016). In another investigation related to Latin America, Key Energy Services, Inc. (Key Energy) settled with the SEC over allegations that its Mexican subsidiary engaged a consulting firm without approval to channel improper payments to an employee of Mexico's state-owned oil company, Petróleos Mexicanos (PEMEX). Because Key Energy was reportedly on the verge of bankruptcy at the time of its settlement, the SEC only required $5 million in disgorgement and did not impose a civil penalty. In September, the SEC entered into a $6 million FCPA settlement with Belgium-based brewing company Anheuser-Busch InBev (AB InBev) over alleged improper payments, routed through third-party sales promoters, to government officials in India to increase sales and production.

The SEC brought its largest corporate enforcement action of the quarter in September, settling with New York-based hedge fund Och-Ziff Capital Management Group LLC (Och-Ziff) for nearly $200 million, as part of a $412.1 million joint resolution with the DOJ. The agencies alleged that Och-Ziff funded transactions by intermediaries, agents, and business partners in which bribes were paid to high-level government officials in several African countries, including officials with Libya's sovereign wealth fund, as a means to secure investments and mining rights and otherwise influence relevant officials.

The three individuals resolving FCPA-related charges with the SEC this quarter include two C-suite executives of an issuer company and a senior-level executive of an issuer's Chinese subsidiary. In mid-September, the SEC entered into an administrative settlement with Jun Ping Zhang (Ping), a former executive with Florida-based technology-services firm Harris Corp. (Harris) and former CEO and Chairman of its Chinese subsidiary, who agreed to pay a $46,000 penalty in connection with alleged payments the subsidiary had made to certain customers, potential customers, consultants, and government regulators. The SEC announced the enforcement action against Ping, together with its decision to decline enforcement against Harris, following a declination the company received from the DOJ in May 2016 (see Declinations section below and our FCPA Summer Review 2016). Later the same month, the SEC entered into administrative settlements with Och-Ziff CEO Daniel Och and CFO Joel Frank to resolve charges that the two men had allegedly ignored red flags in authorizing the illicit transactions at issue in the SEC and DOJ actions against Och-Ziff. Och agreed to pay a nearly $2.2 million penalty as part of his settlement, while the penalty to be imposed against Frank is still under consideration by the Commission.

A development likely to facilitate the SEC's enforcement of the FCPA against individual defendants is a September 30th decision from the U.S. District Court for the Southern District of New York in the SEC's ongoing civil action against three former executives of Magyar Telekom, Plc (Magyar). The court's decision affirmed two jurisdictional theories that largely favor the SEC in FCPA cases against foreign executives. First, the court held that it has personal jurisdiction over the three Hungary-based executives based on their roles in the preparation of Magyar's SEC filings. The court found that representations the defendants made to the company's independent auditor in connection with Magyar's financial disclosures and other securities filings that were ultimately submitted via the SEC's EDGAR website satisfied the requisite "minimum contacts" for personal jurisdiction over the defendants in the United States. The court concluded that its exercise of personal jurisdiction was reasonable, notwithstanding burdens alleged by the defendants, because the SEC's suit furthered a significant interest in enforcing U.S. securities laws and because the litigation would not interfere with other countries' enforcement of their own laws. Second, the court held that the SEC satisfied the "use of instrumentality of interstate commerce" element of the anti-bribery statute, ruling that the defendants' participation "in the preparation of falsified SEC filings that were posted to and accessible from the SEC's EDGAR internet web site" constituted use of an instrumentality of interstate commerce, and finding that Magyar's filings with the SEC were a foreseeable consequence of defendants' actions. By establishing jurisdiction over foreign individuals based solely on their roles in helping prepare a company's securities filings, the court contributed to the SEC's broad view of its jurisdiction under the FCPA. This decision increases the SEC's leverage in future negotiations with individual targets of FCPA investigations and could embolden the SEC in the pursuit of non-U.S. nationals under the statute going forward.

Significantly, all of the SEC's enforcement actions this quarter were brought via administrative proceeding, which continues a trend we have discussed in several recent FCPA Reviews. We expect this pattern to continue, as the SEC has vigorously defended its use of administrative tribunals in the face of constitutional challenges by defendants (see our FCPA Summer 2016 Review). Of note, the U.S. Court of Appeals for the District of Columbia Circuit recently sided with the SEC on this issue, finding the appointment process for SEC Administrative Law Judges (ALJs) to be constitutional. We discuss this opinion below, as well as the SEC's amended Rules of Practice, which went into effect on September 27, 2016.

The DOJ's three corporate FCPA dispositions this quarter all featured parallel SEC actions, described above. The first of these settlements, a three-year Deferred Prosecution Agreement (DPA) with LATAM, was based on alleged misconduct by the company's subsidiary LAN in Argentina. The other two enforcement actions - a three-year DPA with Och-Ziff and a guilty plea by Och-Ziff's wholly-owned subsidiary OZ Africa Management GP LLC - were triggered by alleged misconduct in Africa by the two companies.

SEC and DOJ Enforcement Trends

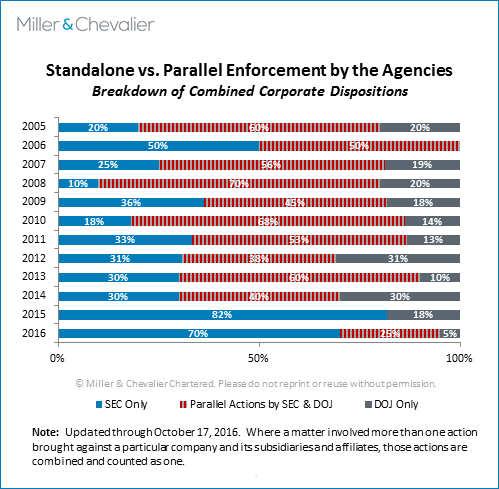

Historically, the SEC and DOJ have, on balance, resolved comparable numbers of FCPA corporate enforcement actions each year, particularly when counting distinct actions against affiliated corporate entities as a single resolution. Since 2015, however, this balance has shifted, with the SEC entering into more than three times as many combined corporate dispositions as the DOJ during the same time frame. This shift likely reflects the strategic decision by the DOJ to reallocate internal resources within the Department toward focusing on larger, high-impact cases and on pursuing culpable corporate executives.

The following chart, which tracks the percentage of combined corporate enforcement actions brought by each agency since 2005, captures this evolving trend, detailing how the SEC's enforcement role vis-à-vis the DOJ has morphed in recent years. The historically large percentage of parallel enforcement actions brought by both agencies highlights the fact that most government-driven FCPA investigations initially involve both the SEC and DOJ, except where the investigation target is not an issuer. As these investigations unfold, however, one of the agencies sometimes decides against pursuing a parallel action. There could be many reasons for this, including but not limited to: a determination by the DOJ that the elements of a criminal violation have not been met; particular facts that deprive either the DOJ or SEC of jurisdiction; recognition that a particular case is better suited for one agency or the other; or a decision by an agency to decline enforcement in recognition of a company's voluntary self-disclosure, extraordinary cooperation, or remedial compliance measures.

As this chart illustrates, the SEC has consistently been involved in approximately 70 to 90 percent of all the corporate FCPA dispositions over the last 11 years, with the figure rising to 95 percent for the first nine months of 2016. Through 2014, the DOJ was involved in a comparable number of enforcement actions - approximately 60 to 80 percent of the total number of combined corporate resolutions - but that figure dropped significantly to 18 percent in 2015 and 30 percent in 2016 to date. Notably, the share of resolved enforcement actions involving the DOJ has declined in tandem with a decline in the DOJ's participation in parallel resolutions with the SEC.

It is important, however, not to make too much of the overall number of corporate enforcement actions brought by the SEC and DOJ each year, as this is not the only meaningful metric of the agencies' enforcement activity. For instance, this measurement does not:

- include the prosecution of individuals on FCPA-related counts, where the DOJ has outpaced the SEC in recent years and which is an area of particular DOJ emphasis, especially in light of the Yates Memorandum;

- account for the DOJ's and SEC's wide-reaching investigative efforts, which often do not result in enforcement actions but nevertheless represent a significant investment of resources by the agencies;

- consider DOJ initiatives such as the FCPA pilot program, which promises participants who self-disclose and cooperate benefits up to and including a declination; or

- take into consideration the size and scope of the agencies' respective corporate resolutions, instead treating them all as equals.

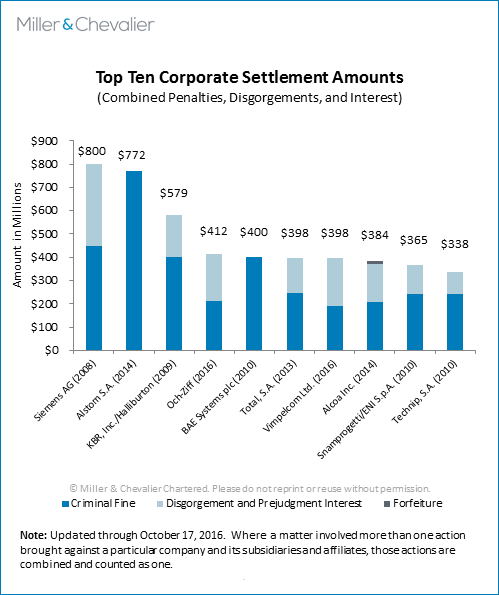

In 2016, for example, two of the agencies' corporate resolutions resulted in combined settlement amounts that rank among the top ten largest enforcement actions of all time by dollar value, specifically the agencies': (1) February 2016 settlement with VimpelCom Ltd. (VimpelCom) and one of its subsidiaries, which imposed penalties, disgorgement, and interest totaling almost $398 million; and (2) September 2016 settlement with Och-Ziff and a subsidiary, which resulted in penalties, disgorgement, and interest totaling approximately $412 million. The chart below details the top ten largest corporate FCPA settlements, which has been updated to include both the VimpelCom and Och-Ziff settlements.

The magnitude of these recent settlements, as well as the DOJ's involvement in fewer corporate resolutions overall, bear out the Department's stated intent to move way from "smaller cases" toward "bigger, higher impact cases," which we discussed in our FCPA Winter Review 2016. The growing number of resolutions by the SEC, most of which have involved smaller-value settlements, further illustrate the growing divergence of the agencies' FCPA enforcement paradigms over the last two years.

Declinations

While declinations traditionally refer to the DOJ or SEC closing an active FCPA investigation without enforcement and without any reciprocal agreement by the target company, the DOJ issued a new type of declination to two companies in September, representing a hybrid approach to the resolution of FCPA investigations. These declinations, provided to NCH Corporation (NCH) and HMT LLC (HMT), were released in the form of "letter agreements" from the DOJ that contained the respective company's signature and set forth facts and conditions to which each company agreed.

Heretofore, declinations, at least in the FCPA context, generally have been simple notices issued by the DOJ to inform target companies of the closure of an investigation - they imposed no conditions or requirements and contained little in the way of analysis. The declinations with disgorgement are, by contrast, essentially a new form of settlement that represents a cross between a traditional declination and a typical settlement, since they require the target company's formal consent to a series of conditions, including the public disclosure of wrongdoing, disgorgement of all profits made from the illegal conduct, and continued cooperation in ongoing investigations of individuals, in exchange for the Department agreeing to decline prosecution. However, these declinations with disgorgement would seem preferable for companies' to their closest analog, the non-prosecution agreement (NPA), for several reasons, including the absence of common NPA requirements such as monetary penalties, directed compliance program enhancements, periodic self-reporting obligations, and broader cooperation expectations.

Due to their unique nature, we review the declinations against NCH and HMT in a separate article below. Notwithstanding the substantive distinctions from historical declinations and other forms of settlement such as NPAs, we have counted these declinations with disgorgement as declinations in our statistics since the DOJ characterizes them as such, but we have and will distinguish them in the future, as appropriate.

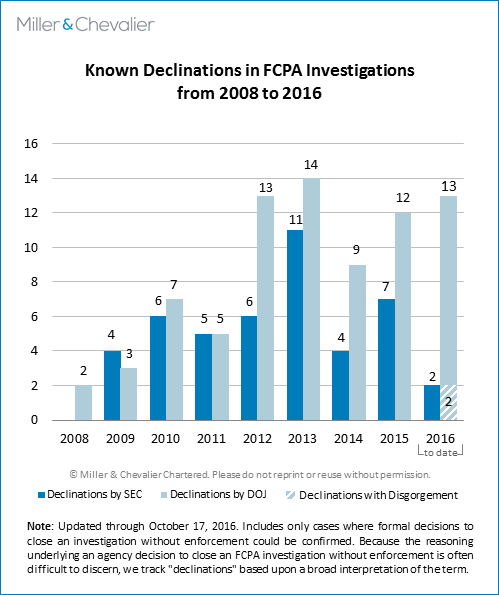

Including the declinations against NCH and HMT, the agencies issued 10 known declinations this quarter, including eight by the DOJ and two by the SEC. The DOJ's 13 declinations to date this year, which already exceeds last year's total, likely have contributed to the recent drop in DOJ enforcement actions, discussed in the preceding section.

The DOJ has issued a significant number of its recent declinations -- two last quarter and three this quarter, including those issued to NCH and HMT -- under its FCPA pilot program. Introduced in April 2016, the pilot program seeks to encourage self-disclosure of potential FCPA violations and greater cooperation by companies in exchange for greater leniency by the DOJ. In our FCPA Summer Review 2016, we noted that the DOJ's public release of declination letters under the pilot program broke with the historical practice of informing only the target company of a declination. Until this time, the ability to track declinations was largely dependent on whether the recipient companies chose to make their declinations public; for example, if they concluded they were required to do so under securities laws. In contrast, under the pilot program the DOJ has begun, at least in certain instances, to publicly release its declination letters and has even created a webpage dedicated to this purpose. The Department's public release of these letters appears to serve two purposes - increasing the transparency of its declination process and promoting the purported benefit for companies of taking advantage of the pilot program.

Following is a list of the declinations we identified this quarter. Of note, while the SEC opted to pursue enforcement in several of the investigations the DOJ declined to prosecute, the DOJ, for its part, joined the SEC in declining enforcement in both investigations where the Commission issued declinations this quarter:

- Johnson Controls: On July 11, 2016, the Wisconsin-based industrial company entered into a disposition with the SEC over alleged violations of the FCPA's books-and-records and internal-accounting-controls provisions (see below). On the same day, the DOJ publicly released a declination letter announcing the Department's decision to close its inquiry into possible FCPA violations by the company "consistent with the FCPA Pilot Program" and "despite the bribery by employees of [the company's] subsidiary in China." The letter identifies several factors as the basis for the declination, including the company's: (1) voluntary self-disclosure; (2) thorough investigation; (3) full cooperation, including "provision of all known relevant facts about the individuals involved in or responsible for the misconduct," and "agreement to continue to cooperate in any ongoing investigation of individuals"; (4) steps taken to enhance its compliance program and internal accounting controls; (5) full remediation, including separation of all employees found to be involved in the misconduct; and (6) payment of full disgorgement and a civil penalty to the SEC.

- AB InBev: In an SEC filing on August 29, 2016, the Belgian brewing company disclosed that the DOJ had notified the company on June 8, 2016 that the Department was closing its investigation "into AB InBev's current and former affiliates in India ... and whether certain relationships of agents and employees were compliant with the" FCPA, and that the DOJ "would not be pursuing enforcement action in this matter." The filing indicated, however, that the SEC's investigation was ongoing. On September 28, 2016, AB InBev and the SEC entered into a settlement over the company's alleged violations of the books-and-records and internal-accounting-controls provisions of the FCPA and the whistleblower protection provisions of the Dodd-Frank Act (see below).

- AstraZeneca: On August 30, 2016, the biopharmaceutical company entered into a settlement with the SEC, based on alleged deficiencies in the company's internal accounting controls (see below). In connection with the SEC settlement, the company announced that the Commission acknowledged the company's "cooperation during the entire course of the inquiry" and that the DOJ had closed its parallel investigation into the underlying activities in China and Russia by the company's subsidiaries.

- Cisco Systems, Inc. (Cisco): In its Form 10-K filed on September 8, 2016, the California-based networking technology company announced that the SEC and DOJ had "recently informed [the company] that they have decided not to bring enforcement actions" based on the results of the "investigation into allegations which [Cisco and the SEC and DOJ] received regarding possible violations of the [FCPA] involving business activities of [the company's] operations in Russia and certain of the Commonwealth of Independent States, and by certain resellers of [Cisco] products in those countries." The company further stated that it had "fully cooperated with and shared the results of [its] investigation with the" agencies. Cisco previously disclosed this investigation in a Form 10-Q filed with the SEC on February 20, 2014.

- Harris: In the September 12, 2016 release announcing the SEC's settlement with Ping, the Commission disclosed that it had "determined not to bring charges against Harris, taking into consideration the company's efforts at self-policing that led to the discovery of Ping's misconduct shortly after the acquisition, prompt self-reporting, thorough remediation, and exemplary cooperation with the SEC's investigation." The DOJ had previously advised the Florida-based technology services company of its decision to decline enforcement of the same underlying conduct in May 2016, as described in our FCPA Summer Review 2016.

- HMT: On September 29, 2016, the DOJ publicly released its letter to the Texas-based manufacturer of above-ground storage tanks, announcing that the Department was closing its FCPA investigation of the company "[c]onsistent with the FCPA Pilot Program announced April 5, 2016." As noted in our discussion of the declinations issued to NCH and HMT below, the DOJ's investigation reportedly found a number of FCPA violations relating to the company's sales in Venezuela and China; however, the Department chose to close the investigation under the FCPA pilot program due, in part, to NCH's self-disclosure, thorough internal investigation, cooperation, steps taken to enhance its compliance program and internal accounting controls, full remediation, and the company's agreement to disgorge $2,719,412, "which represents the profit to HMT from the illegally obtained sales in Venezuela and China."

- NCH: On September 29, 2016, the DOJ publicly released its letter to the Texas-based industrial supply and maintenance company, which largely mirrored the DOJ's declination letter to HMT and announced that the Department was closing its FCPA investigation of NCH and its subsidiaries "[c]onsistent with the FCPA Pilot Program." As noted in our discussion of the declinations issued to NCH and HMT below, the DOJ's investigation reportedly found a number of FCPA violations stemming from conduct of NCH's subsidiary in China. According to the DOJ's declination letter, the Department chose to close the investigation under the FCPA pilot program due, in part, to NCH's self-disclosure, thorough internal investigation, cooperation, steps taken to enhance its compliance program and internal accounting controls, full remediation, and the company's agreement to disgorge $335,342, "which represents the profit to NCH from the illegally obtained sales in China."

- Glaxo: On September 30, 2016, the same day the SEC announced that it had reached a settlement with Glaxo over alleged accounting violations in China, the U.K. pharmaceutical company informed press outlets that: "The [DOJ] has also concluded its investigation into these matters and will be taking no further action." The DOJ, for its part, has declined to comment on this matter.

- Grifols SA (Grifols): In its Form 6-K, filed with the SEC on October 7, 2016, the Spanish pharmaceutical company stated that the DOJ "notified Grifols that the Department has closed its inquiry into Grifols, concerning possible violations of the U.S. Foreign Corrupt Practices Act." The company's disclosure further notes that "[i]n its notice of declination to prosecute, the Department acknowledged the full cooperation of Grifols in the investigation."

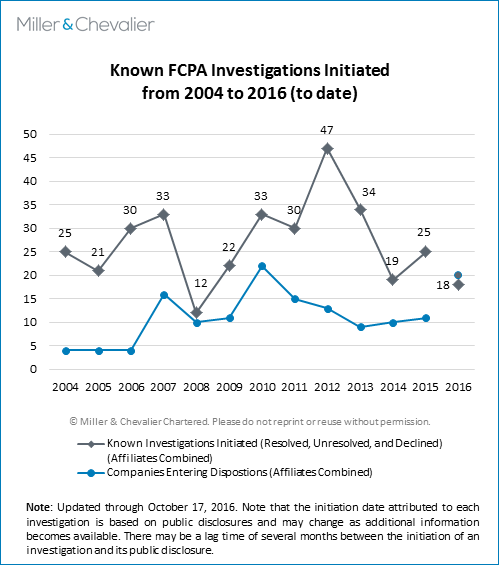

Known Investigations

In addition to the 38 enforcement actions resolved by the SEC and DOJ during the first three quarters of the year, we have identified 18 new FCPA investigations initiated by the agencies in 2016 to date, suggesting an active level of overall FCPA enforcement activity. By comparison, at this point in 2015, we had identified 17 investigations initiated by the SEC or DOJ alongside the 19 enforcement actions the agencies had brought during the first three quarters of the year.

Since the publication of our FCPA Spring Review 2016 in May, we have identified 12 additional FCPA investigations initiated by the agencies in 2016, as well as two previously unknown investigations initiated prior to this year. As we have noted in prior Reviews, the DOJ and SEC almost certainly have a significant number of FCPA investigations underway that are not yet public knowledge because the agencies and the companies involved have chosen not to publicly disclose them at this time. The numbers in the chart are therefore likely to rise, even for past years, since public companies sometimes wait months, or even years, to disclose the existence of an investigation in their securities filings - with some choosing never to do so - and non-issuer companies often never disclose the existence of an investigation. However, with the DOJ beginning to publicize more of its declination decisions, as discussed in the Declinations section above, the public is bound to learn of FCPA investigations that, in the past, may never have been publicly disclosed. For example, the DOJ's decision to publicly divulge the declinations it provided to HMT and NCH in September represented the first public acknowledgement of these investigations, which we have now updated the chart above to reflect.

International Developments

The past quarter also saw a number of relevant international developments. In Great Britain, the U.K. Serious Fraud Office (SFO) entered into its second-ever DPA on July 8, 2016, reaching a settlement with an unnamed U.K. enterprise over allegations of foreign bribery. The DPA includes a charge of failure to prevent bribery under the U.K. Bribery Act 2010 (UKBA), and a charge of conspiracy under the Criminal Law Act of 1977, which applies to conduct that occurred before the UKBA entered into force in 2011.

In Brazil, a review board within the Federal Public Prosecutor's Office rejected a settlement between Brazilian authorities and Dutch oil-services firm SBM Offshore (SBM) related to SBM's alleged bribery of executives at Petróleo Brasileiro S.A. (Petrobras), Brazil's national oil company. SBM had agreed to pay over $340 million to Petrobras and the Brazilian government as part of the settlement, but the settlement is now on hold, pending review by a higher level review panel within the Federal Public Prosecutor's Office. The corruption investigation of Petrobras continues to ensnare additional Brazilian political figures, with corruption charges filed against former President Luiz Inácio Lula da Silva and the arrest of former Finance Minister Guido Mantega. In addition, the Brazilian Senate voted to convict President Dilma Rousseff, concluding her impeachment proceeding, and, less than two weeks later, the Brazilian Chamber of Deputies voted to expel its member and former Speaker Eduardo Cunha on account of money laundering and corruption allegations.

Meanwhile in Mexico, the country's president signed new anti-corruption legislation into law on July 18, 2016, implementing the 2015 Constitutional reform on anti-corruption. The legislation creates a coordinating committee responsible for managing the development of anti-corruption guidelines at all levels of Mexico's government, and includes provisions aimed at public officials and private sector corruption, including new disclosure requirements and broadened sanctions and penalties.

Actions Against Corporations

Johnson Controls Settles with the SEC over Alleged FCPA Accounting Violations in China

On July 11, 2016, Johnson Controls, a Wisconsin-based global provider of building efficiency systems, automotive batteries, and seating and interior systems for automobiles, agreed to pay more than $14 million to the SEC to settle charges that it violated the books-and-records and internal-accounting-controls provisions of the FCPA. According to the Cease-and-Desist Order (Order), between 2007 and 2013, China Marine, the Chinese subsidiary of Johnson Controls' Global Marine building efficiency business, made more than $4.9 million in improper payments. China Marine employees allegedly used the improper payments to obtain and retain business and for personal enrichment. The Order stated that, as a result, Johnson Controls' books and records did not accurately and fairly reflect Johnson Controls' transactions and disposition of its assets. Many Johnson Controls vendor payments "were incorrectly recorded as legitimate vendor transactions … when in fact they were payments for goods never received or payments intended for foreign or commercial bribery or embezzlement."

The scheme came to light in 2013 after Johnson Controls received anonymous reports following the departure of China Marine's managing director. After becoming aware of the allegations, Johnson Controls quickly and voluntarily disclosed the allegations to the U.S. authorities -- about one month after receiving the second anonymous tip. Johnson Controls then extensively cooperated with the SEC and the DOJ's investigation. At around the same time as the SEC settlement, the DOJ publicly disclosed that it has declined to prosecute Johnson Controls for China Marine's alleged conduct, "consistent with the FCPA Pilot Program."

The same Chinese operation was implicated in York International's (York) 2007 FCPA settlement, which Johnson Controls acquired in 2005 (see discussion in our FCPA Autumn Review 2007). The 2007 SEC Consent Judgment alleged that York's Chinese subsidiary, China Marine's predecessor, provided high-value gifts to Chinese shipyard employees and paid its agents "hundreds of thousands of dollars for nebulous and undocumented services." According to the SEC, after Johnson Controls acquired York in 2005, Johnson Controls investigated York's business practices in China, terminated individuals involved in the alleged misconduct at China Marine, hired a new managing director of China Marine, and limited China Marine's use of agents and required that all sales go through China Marine's internal sales team based in China.

But, according to the recent SEC Order, China Marine employees, including the new managing director, "devised another avenue to continue the [improper] payments." The SEC alleged that instead of diverting funds using agents, who now faced more stringent scrutiny under Johnson Controls' compliance program, China Marine used vendors, who Johnson Controls considered lower risk and were subjected to less due diligence and monitoring. According to the SEC, Johnson Controls considered China Marine vendors lower risk because (1) the vendors did not interface with government officials and (2) the vendors generally had low-dollar-value transactions with China Marine. By using inflated or fake vendor transactions that averaged only $3,400 each, China Marine employees were able to divert the $4.9 million used for the alleged improper payments in the course of the six-plus-year period.

Among other purposes, China Marine employees allegedly used funds generated by their illicit scheme to pay "employees of government-owned shipyards … to obtain and retain business ..." The new vendor scheme, according the SEC, was a "multi-stepped arrangement" that involved collusion among the managing director, 18 other China Marine employees from three offices and several China Marine vendors. The managing director allegedly approved adding vendors to the vendor master file without disclosing that certain sales managers had beneficial interests in these vendors. As a result, the sales managers allegedly added fake costs for parts and services to sales reports, thereby inflating project costs. Procurement managers allegedly "knowingly" approved bogus purchase orders and the vendors, allegedly, "at the direction of China Marine sales managers, created fake order confirmations … and invoices." Finally, the finance manager allegedly authorized payments "even when supporting documentation was missing or erroneous." According to the SEC, funds generated through these fake transactions were transferred to China Marine employees' personal bank accounts and then used for bribery and personal enrichment.

The SEC's Order highlighted Johnson Controls' lack of oversight as the main internal controls failure that allowed the extensive scheme to go undetected for over six years. According to the Order, this lack of oversight manifested in three ways:

- Johnson Controls had "very little oversight" of China Marine's operations and instead relied on the newly-hired managing director's "ability to self-police" his business operations. The company did not review most China Marine vendor transactions, because the average vendor payment was $3,400, significantly below the threshold that would trigger review by Johnson Controls' Denmark office, which oversaw its Global Marine business. Similarly, Johnson Controls did not ensure that audits would adequately review vendor payments that were below the "audit testing threshold."

- Even when Johnson Controls reviewed vendor transactions, such as when a transaction met the review threshold or during audits, its managers based in Denmark admitted that "they did not have sufficient knowledge and understanding of China Marine's projects to recognize when certain vendor payments were unnecessary, whether goods ordered had actually been delivered, or whether design fees were necessary given [Johnson Controls] had an in-house design service."

- The lack of oversight by headquarters allowed a "culture of impunity" to exist at China Marine.

The alleged illicit scheme began while York/Johnson Controls was still under its three-year monitorship from the 2007 settlement. The original remediation arising from the first settlement clearly failed, and particularly relevantly, the SEC's Order noted that Johnson Controls failed to implement adequate controls in spite of the prior settlement and in spite of a recommendation by the compliance monitor that the company "integrate the [China] Marine business more closely into [Johnson Controls'] compliance culture." Yet, the SEC settled with Johnson Controls in an administrative proceeding in which the company was not required to admit to any of the Commission's findings and was not required to retain a monitor. Furthermore, the DOJ declined to prosecute the company. The DOJ's declination letter explicitly referenced its pilot program. The DOJ also publicly released the declination letter, adding to an apparent recent trend toward publicizing declinations (see discussion in our FCPA Summer Review 2016). Both the DOJ declination letter and the SEC Order made it clear that Johnson Controls has met all the conditions set forth by the pilot program for lenient treatment such as no requirement for a monitor or declination. These factors suggest that the agencies' programmatic goals may have played a role in the seemingly unusually favorable outcome Johnson Controls was able to secure in this case despite China Marine being a repeat offender. Johnson Controls' specific cooperation and remediation actions highlighted by the DOJ in its declination letter include the following:

- voluntary self-disclosure;

- thorough investigation by the company;

- full cooperation, with an emphasis on the "provision of all known relevant facts about the individuals involved in or responsible for the misconduct" and the company's "agreement to continue to cooperate in any ongoing investigation of individuals";

- steps taken to enhance the company's compliance program and internal accounting controls;

- full remediation, including separation from all employees found to be involved in the misconduct; and

- payment of full disgorgement and a civil penalty to the SEC.

Noteworthy Aspects

- No "Low-Risk" Third Parties in High-Risk Markets: The facts of this case highlight what many practitioners know from experience: there are no truly low-risk third parties in high-risk markets. Johnson Controls tightened its controls on agents, so China Marine local management created slush funds using vendors, which Johnson Controls erroneously believed posed lower risk. As a result, Johnson Controls did not sufficiently vet and monitor China Marine vendors. While the SEC's Order did not discuss the exact nature of China Marine's allegedly bogus or colluding vendors, they appear to have been design companies and other vendors involved in China Marine's core business. In our experience in China, we have seen many mundane vendors traditionally considered low risk used for diverting funds for illicit purposes, including: printing and stationary vendors, car rental companies, office equipment vendors, catering companies, advertising companies, and building materials vendors. Some of these types of vendors in China have been involved in other FCPA dispositions. Johnson Controls' experience cautions that, in risk-balancing a compliance program, while it is common practice to establish lower due diligence and monitoring requirements for lower-risk third parties, in high-risk jurisdictions like China, even traditionally low-risk third parties often warrant higher scrutiny.

- Effective Monitoring Needs to Be Informed and Probing: Johnson Controls employees and auditors reviewed some of China Marine's vendor transactions, but failed to detect the improper payments. Indeed, they admitted to investigators that they did not have "sufficient knowledge and understanding of China Marine's projects to recognize when certain vendor payments were unnecessary, whether goods ordered had actually been delivered, or whether design fees were necessary given Johnson Controls had an in-house design services." Without a doubt, asking such detailed and probing questions in vetting or auditing a third party is time consuming for compliance personnel and auditors and potentially uncomfortable because it could involve interrogating trusted local managers. This task is even more difficult if the company's business is complex or highly technical. But the monitoring failures discussed in the SEC's Order show that vetting and monitoring third-party relationships in high-risk markets (as well as managing other key compliance risks) must involve understanding the local business in depth and, for at least a selection of transactions reviewed, asking detailed and probing questions similar to those highlighted by the SEC and quoted above. This testing is particularly important for transactions for which reviewers and auditors, based on normal supporting documents alone, could not ascertain the legitimacy of the transaction.

LATAM Airlines and LAN Airlines Settle with SEC and DOJ Related to Argentinian Operations

On July 25, 2016, the DOJ and the SEC announced that they reached agreement with LATAM and LAN, respectively, to settle FCPA books-and-records and internal-accounting-controls violations. LAN was a publicly-traded airline company headquartered in Santiago, Chile, that provided passenger and cargo airline services throughout Latin America and its common stock was registered on the New York Stock Exchange. LATAM is the successor-in-interest to LAN. LAN became LATAM after a 2012 merger with TAM Airlines S.A. and LATAM's holdings now include LAN and its subsidiaries.

The airline agreed to pay more than $22 million to settle parallel civil and criminal cases related to improper payments it authorized during a dispute between the airline and its union employees in Argentina. This case is related to SEC's February 2016 settlement with Ignacio Cueto Plaza, which we discussed in our FCPA Spring 2016 Review. Ignacio Cueto Plaza was LAN's then-President and COO and is currently LAN's CEO.

The DOJ entered into a three-year DPA with LATAM to settle a two-count charge of violating the internal-accounting-controls and the books-and-records provisions of the FCPA. As part of the DPA, LATAM agreed to pay a $12.75 million criminal penalty, to continue to cooperate with the DOJ's investigation, to enhance its compliance program and to retain an independent compliance monitor for a term of at least 27 months.

For its part, the SEC filed a Cease-and-Desist Order charging that LAN failed to keep accurate books and records and maintain internal accounting controls. LAN will pay $6.74 million in disgorgement and $2.7 million in prejudgment interest.

According to the SEC and DOJ documents, following several years of exploring potential expansion into Argentina, LAN entered the Argentine market in 2005 by purchasing 49 percent of the shares of AERO 2000. AERO 2000 was a non-operating Argentine airline that possessed an airline operation certificate and owned flight routes. As part of the deal, LAN agreed to hire workers from two defunct Argentine airlines.

Around 2006, the labor unions representing those workers began making demands on LAN Airlines. For example, the unions each had a "single-function" rule in their collective agreements with the airlines that limited workers from performing more than one work function for LAN. The unions did not enforce this rule and if they were to do so, LAN would have to double its work force, which would have seriously imperiled its ability to continue operations in Argentina. In 2006, the unions began campaigning for wage increases and they threatened to enforce the single-function rule unless LAN Argentina agreed to a substantial wage increase.

The DOJ and SEC documents allege that, in 2006 and 2007, LAN executives authorized payments to an Argentine consultant knowing that the consultant might pass some portion of the money to union officials in Argentina to help settle the dispute with the unions. At that time, the papers allege, the consultant was a "Cabinet Advisor 'ad-honorem'" to Argentina's Secretary of Transportation.

The consultant allegedly provided LAN executives with information on how to deal with specific unions, provided information on unions in general, and offered to negotiate with the unions directly. However, the draft contract with the consultant, which was never signed, allegedly said the consultant would perform a study of existing air routes in Argentina and the regional market. According to the disposition documents, executives at LAN approved the consultant's compensation and directed the company's CFO to pay three invoices submitted by the consultant totaling $1.15 million and referencing a contract signed by the parties. The DOJ and SEC allege that an unrelated LAN subsidiary, AAI, based in Delaware, made the improper payments on behalf of LAN, which AAI described as payments to "other debtors" on its books and records. The consultant and his wife received the $1.15 million in payments into their brokerage accounts in Virginia. In addition, LAN also paid an additional $58,000 invoice issued by a company owned by the consultant's son and wife that said it was for a study of existing air routes in Argentina and the regional market, which the LAN executives allegedly knew was inaccurate.

In sum, as a result of the sum of these payments, the SEC Cease-and-Desist Order states that LAN obtained a benefit of almost $7 million.

The government's charges do not relate to anti-bribery violations and thus do not explicitly state whether the improper payments in question relate to the payments made by the company to the consultant, or to the payments passed on by the consultant to the unions (the latter option would suggest that the government viewed the unions as foreign officials under the FCPA). However, the DPA states that LAN entered into the $1.5 million consulting agreement with the Consultant "in order to funnel bribes to labor union officials." As a result of these corrupt payments, LAN's unions had agreed not to enforce the one function rule for a period of years and had accepted substantially lower wage increased than they had been demanding. The SEC has similar language, noting that when approving payments to the consultant, LAN "understood that it was possible the consultant would pass some portion of the $1.15 million to union officials in Argentina." At the same time, the consultant himself was a government official by virtue of his position as a cabinet adviser to the Secretary of Transportation, and the SEC faulted LAN for failing to conduct proper due diligence through which "LAN might have become aware of his January 2005 appointment as a Cabinet Advisor to Argentina's Transportation Secretary."

Noteworthy Aspects

- No Bribery Violations Brought: Neither the DOJ nor SEC brought anti-bribery charges in this case, although the government's factual narrative refers to "corrupt" payments. The agencies never identified the union leadership as foreign officials, nor do they identify the consultant as a "foreign official," despite his "Cabinet Advisor 'ad-honorem'" role to Argentina's Secretary of Transportation. Presumably his role in government offered some benefit to LATAM in the negotiation process with the unions, but it was not sufficient to allege bribery. Alternatively, the government might have faced evidentiary hurdles which precluded it from building an effective bribery case; for example, there is a reference in the DPA that "because of the [company's] delayed disclosure, potentially relevant evidence was lost or destroyed, including the routine application of data retention policies."

- Lack of Sufficient Remediation: In listing out the factors the Department considered in entering into the DPA, it noted that LATAM has designed and is in the process of implementing a compliance program and system of internal accounting controls and has committed to ensuring that these will continue to be implemented in a sufficient manner. However, at the same time, the DOJ noted that the "[c]ompany has failed to remediate adequately, including significantly by failing to discipline in any way the employees responsible for the criminal conduct recounted in the statement of facts … including misconduct by at least one high-level Company executive and thus the ability of the compliance program to be effective in practice is compromised." This language is unique and suggests that the DOJ questions whether effective remediation is possible so long as senior executives of concern remain in their positions.

- Potential Action Against Other Individuals: While the DOJ and SEC have not released any statements related to any pending charges against additional employees, the disposition documents indicate that there might be at least one additional case. For example, the documents extensively refer to LAN's Vice President of Business Development who is a U.S. citizen residing in Miami, Florida. While the documents do not indicate any specific wrongdoing on behalf of this employee, he or she was in charge of LAN's expansion efforts into Argentina and was involved in some of the underlying facts of the case. However, given how historic the underlying allegations are, it is also likely that any cases would have been brought already.

- First Enforcement Action Against South American Company: The DOJ and SEC's parallel enforcement against LAN and LATAM represent the first FCPA- related enforcement action against a company that is headquartered in South America. While there have been enforcement actions against companies' Latin American subsidiaries such as in Ralph Lauren Corporation and Stryker Corporation, or where the improper payments were made to officials in South America, such as in BizJet, this is the first instance where the U.S. government brought charges against a South American company. Surprisingly, the first Latin American-based company to settle FCPA charges is from Chile, a country traditionally perceived to be less corrupt than other countries in the region; for example, in Miller & Chevalier's 2016 Latin America Corruption Survey, Chile was in the top three countries for survey participants' perceptions of the effectiveness of its anti-corruption laws. However, the activity in question occurred in Argentina, a country that scored significantly worse than Chile in the same survey results; for example, survey results indicated that only three percent of survey participants in Argentina believe that their country's anti-corruption laws are effective. It is likely that LATAM won't have the distinction of being the only Latin American company with an enforcement action against it for long, as earlier this month Brazilian aircraft manufacturer Embraer S.A. reported a $200 million pre-settlement reserve and several other investigations of South American companies, including Petrobras and Eletrobras (both Brazilian) and Sociedad Quimica y Minera S.A. (Chilean) have been made public.

- Pilot Program: Although the DOJ's new pilot program is not referenced in the settlement documents, it is likely that the DOJ did not view this case eligible for that program. This is likely because as the DPA states, LAN "did not timely voluntarily disclose the FCPA violations to the Office," and only did so after press reports surfaced that local enforcement officials had commenced investigations of the conduct. The pilot program does give limited credit for companies who do not voluntary self-disclose, but only if they appropriately remediate; in this case, as discussed above, the DOJ documents indicate that they do not consider the company's remediation efforts satisfactory, in part due to not disciplining "employees responsible for the criminal conduct." Nevertheless, the company's cooperation was significant enough to receive two points off of its culpability score, which helped reduce its penalty in the final fine calculation. However, it would have presumably been entitled to greater discount or possibly a declination for the accounting provision violations had there been earlier disclosure or better remediation.

- Unique Monitor Term Length: We are not aware of another settlement resulting in a monitor term lasting 27 months. The most common lengths are one, two, or three years in duration. Several settlements also have a hybrid arrangement with an 18-month independent monitorship and an 18-month self-monitorship. LATAM's DPA length is three years.

- Local Enforcement Unclear: The DPA states that Argentine and Chilean law enforcement officials had commenced investigations of the conduct in question. South American media has reported that Argentine authorities are investigating former transportation secretary Ricardo Jaime for receiving $1.15 million in bribes from LAN and specifically, whether Jaime accepted bribes through his private secretary, Manuel Vázquez. There are also media reports that Chilean prosecutors have opened a similar investigation relating to bribery of Jaime.

Key Energy Settles with the SEC Over Alleged Payments to Employee of Mexican National Oil Company

On August 11, 2016, Texas-based oilfield-services company Key Energy Services, Inc. settled the SEC's allegations that the company violated the FCPA's internal-accounting-controls and books-and-records provisions. As part of the settlement, Key Energy agreed to pay $5 million in disgorgement - the only monetary penalty imposed on the company.

The SEC's central allegation against the company, detailed in the Commission's Cease-and-Desist Order (Order), is that Key Energy's Mexican subsidiary, Key Mexico, made corrupt payments to an employee at Mexico's state-owned oil company, PEMEX, through a consulting firm.

According to the Order, between 2010 and 2013, Key Mexico hired a consulting firm with ties to an employee at PEMEX to advise the company regarding its contracts with PEMEX. The Order did not elaborate on the nature of these ties. Key Mexico's former country manager approved and carried out this hiring decision. While Key Energy became aware that Key Mexico was doing business with this consulting firm (but not that firm's ties to the PEMEX official) as early as 2011, it allowed Key Mexico to continue working with the firm without a contract and without conducting due diligence, despite having such requirements in the company's compliance program. Moreover, the SEC faulted the company for Key Mexico having no compliance staff or internal audit processes of its own.

According to the SEC, Key Energy received numerous benefits as a result of the payments made to the consulting company. In 2011, before PEMEX had issued certain contracts for tender, the PEMEX employee linked to the consulting company forwarded internal emails from PEMEX officials with information on these contracts to Key Mexico's country manager, who passed them on to Key Energy employees in Houston. One of Key Energy's vice presidents who saw these emails suggested that PEMEX should add $90 million to an ongoing Key Mexico contract. In March 2011, PEMEX amended this contract to increase it by about $60 million.

The SEC alleged that Key Mexico paid the consulting firm approximately $561,000 between 2010 and 2013. Key Mexico's employees entered at least $229,000 of this amount in Key Mexico's accounting systems as "Expert advice on contracts with the new regulation of PEMEX…." However, according to the Order, there was no evidence that the PEMEX employee or the consulting firm to which he had ties provided any legitimate consulting services for Key Mexico. The Order alleges that Key Mexico, in fact, funneled money to the PEMEX employee through the consulting firm, including payments of $8,000 per month starting in 2011, after Key Mexico secured an additional contract with PEMEX.

In addition to its payments to the consulting firm, Key Energy authorized Key Mexico to donate about $118,000 in gifts to PEMEX's annual Christmas celebration in 2012. While Key Energy employees believed that the gifts would be used in a raffle, as they had been in the past, Key Mexico employees gave $55,000 of these gifts directly to the approximately 130 PEMEX officials working in the regions where Key Mexico operated. Key Energy approved this amount in gifts for the raffle even though it was approximately nine times and 26 times more than what the company spent on raffle gifts for PEMEX in 2010 and 2011, respectively.

In January 2014, the SEC contacted Key Energy about possible FCPA violations. In April of the same year, Key Mexico's employees told Key Energy management that the former Key Mexico country manager had pledged to bribe at least one PEMEX employee. Key Energy reported these accusations to the SEC and launched an extensive internal investigation. The company hired a new Chief Compliance Officer (CCO), who instituted a "renovation and enhancement" of the compliance program, including manually reviewing vendors in Mexico, implementing a new business opportunities protocol to help the company better understand the business risks of agents, consultants and other business partners and establishing more advanced controls around payment procedures in countries where Key Energy operates. Remedial measures also included instituting in-person visits to international locations by the CCO, reviewing Key Energy's anti-corruption policy and committing to exiting the Mexican market by the end of 2016. According to the Order, Key Energy cooperated with the SEC during the investigation. In April of 2016, Key Energy announced that the DOJ declined to bring an FCPA action against the company.

Noteworthy Aspects

- The SEC Considered Key Energy's Financial Situation in Determining Penalty: The SEC ordered Key Energy to pay $5 million in disgorgement and did not impose a civil penalty. Disgorgement is usually calculated by the amount of illegal profits that the entity received. The Key Energy resolution, however, is an example of a disgorgement amount that was influenced by a company's overall financial situation. According to the SEC, "in determining the disgorgement amount and not to impose a penalty, the Commission has considered Key Energy's current financial position and its ability to maintain necessary cash reserves to fund its operations and meet its liabilities." In recent years, Key Energy has experienced financial difficulties that reflect the general downturn in the oil and gas sector. The company announced in August 2016 that it expected to file for bankruptcy. The SEC's consideration of Key Energy's financial situation is similar to DOJ's conduct toward logistics firm IAP Worldwide Services, Inc. (IAP), which we covered in the FCPA Summer Review 2015. In IAP's case, the DOJ's NPA allowed IAP to pay its fine in four separate installments because of the company's financial difficulties. Here, despite avoiding a penalty and lowering the disgorgement amount, this matter has proven very costly for Key Energy: in its Form 8K filed on June 15, 2016, Key Energy reported that its costs related to this investigation amounted to around $75 million.

- Corruption Trends in Mexico: The facts alleged by the SEC on the part of both Key Energy and the PEMEX employee reflect the trends identified in in Miller & Chevalier's 2016 Latin America Corruption Survey. Of the major economies (over $100 billion GDP) surveyed, Mexico, along with Venezuela, Argentina, and Brazil, was seen as most corrupt in the region. In addition, Mexican state-owned entities, such as PEMEX, scored poorly, with 74 percent of respondents viewing such entities as significantly corrupt. Numerous past FCPA actions have featured payments to PEMEX officials, including Crawford Enterprises, Inc., Paradigm B.V., Siemens AG, and Hewlett-Packard Mexico. Additionally, according to the Survey, only eight percent of the respondents found Mexico's current anti-corruption laws to be effective compared with a regional average of 23 percent. Mexico amended its anti-corruption laws in the summer of 2016 to expand the coverage of violations and strengthen fines, as summarized in an article below.

AstraZeneca Settles Long-Running Investigation with the SEC

On August 30, 2016, the SEC announced an administrative settlement with AstraZeneca, the London-based, UK-incorporated biopharmaceutical company, for $5.5 million in fines and disgorgement. The SEC's Cease-and-Desist Order alleged that, between 2005 and 2010, AstraZeneca failed to devise and maintain a sufficient system of internal accounting controls and thereby allowed its wholly-owned subsidiaries operating in China and Russia to operate several schemes that provided improper benefits to HCPs at state-owned or -controlled hospitals or medical departments and to falsely record those improper benefits as bona fide business expenses. As is common in SEC administrative settlements without a criminal component, AstraZeneca did not admit or deny the SEC's allegations.

With respect to China, the Order alleged that, between 2007 and 2010, AstraZeneca's wholly-owned subsidiary there (AZ China) provided improper benefits to HCPs "as incentives to purchase or prescribe [AstraZeneca] pharmaceuticals." The improper benefits allegedly included gifts, cash, "maintenance fees," entertainment and speaker fees that in some instances were for "totally fabricated" speaking engagements. In addition, AZ China employees made payments in cash to local officials in 2008 "to get reductions or dismissals of proposed financial sanctions against the subsidiary." Funds for the improper payments were allegedly generated in several ways: through employee expense reimbursements that were inadequately supported or supported by fake tax receipts (fa piao), through fake or inflated invoices from a collusive travel vendor, and through "bank accounts in doctors' names" established by AZ China.

According to the Order, local managers planned and closely tracked the improper payments. Allegedly, AZ China employees and managers "maintained written charts and schedules that recorded the amount of forecasted or actual payments [of improper benefits] that AZ China would make per month or year in numerous regions throughout China." The charts detailed specific benefits provided to specific physicians or particular hospitals or medical departments as designated by specific physicians.

With respect to Russia, the SEC made less detailed but similar allegations that, between 2005 and 2010, AstraZeneca's subsidiaries operating in Russia (AZ Russia) provided "improper incentives," in the form of "gifts, conference support and other means," to government-employed HCPs in connection with sales of AstraZeneca pharmaceutical products. Also similar to China, AZ Russia allegedly kept charts that tracked HCPs, their positions and "their level of influence in making purchasing decisions for the respective entities where they worked and the manner in which they could be motivated to purchase [AstraZeneca] products..."

The $5.5 million AstraZeneca agreed to pay the SEC in settlement is composed of $4.3 million in disgorgement, $375,000 in civil monetary penalty and $822,000 in prejudgment interest. The Order stated that the SEC considered AstraZeneca's cooperation in setting the amount of the civil monetary penalty, and while noting that AstraZeneca did not self-report, the Order praised AstraZeneca's "significant cooperation" and remedial efforts.

Noteworthy Aspects

- Long-Running Investigation Involving Multiple Authorities: AstraZeneca's public filings indicate that the SEC began its investigation against the company in October 2006 and initially focused on the firm's businesses in Italy, Croatia, Russia and Slovakia. In 2010, the DOJ either joined the existing investigation, or initiated a new investigation possibly as a part of the then-ongoing pharma sweep. The long span of the investigation makes this settlement an outlier in terms of investigation duration (see our related discussion here), especially given the relatively small settlement amount, the lack of a concurrent foreign prosecution and the apparent lack of any planned individual prosecutions (no individuals were highlighted in the SEC's Order).

In addition to the countries on which the U.S. agencies focused, the Serbian government indicted the company in 2011 for alleged "improper payments to physicians" at a government cancer institute. We have not found information as to the outcome of the DOJ or the Serbian government investigation. Given the SEC settlement, it is likely that the DOJ has or will decline to prosecute the company. Notably, the SEC's Order did not allege facts sufficient to suggest that the DOJ had jurisdiction over the conduct at issue. - Common Payment Patterns, Two Exceptions: The various types of improper payments and schemes alleged against AstraZeneca are mostly typical of other life sciences cases involving conduct in China: gifts, entertainment, conference support, questionable speakers' fees, colluding travel vendors, etc. One unique alleged payment scheme is that AZ China "establish[ed] bank accounts in doctors' names" to enable the improper payments. Another more important unique feature here is that both AZ China and AZ Russia had allegedly maintained charts detailing the incentive schemes and that those charts were maintained at the organizational level and approved by country-level managers. This allegation may have contributed to the SEC's decision to bring charges against AstraZeneca, the UK parent, in spite of its small role and the fact that there is no allegation that any AstraZeneca employees knew of or approved the alleged schemes.

Nu Skin Enters Administrative Settlement with SEC for Improper Charitable Contribution

On September 20, 2016, Nu Skin Enterprises, Inc. (Nu Skin US), a cosmetic and nutritional supplement company headquartered in Provo, Utah, agreed to pay $766,000 in penalties, disgorgement and prejudgment interest to settle an administrative action with the SEC. The SEC alleged that a charitable contribution made by Nu Skin US's wholly-owned Chinese subsidiary, Nu Skin (China) Daily Use & Health Products Co. Ltd. (Nu Skin China), violated the books-and-records and internal-accounting-controls provisions of the FCPA because it allegedly made the contribution in order to influence a government official.

According to the SEC's Order, Nu Skin China made a donation of one million RMB (approximately $154,000) to a charity chosen by a Chinese Communist party official (Party Official) in order to influence an ongoing investigation into the company's sales practices by a local government agency. A provincial-level Administration of Industry and Commerce (AIC) began an investigation of Nu Skin China's sales practices following an unauthorized 2013 promotional meeting hosted by the company when it did not have a direct selling license or a physical retail store in the city, both of which were required under Chinese law. The AIC informed Nu Skin China that it intended to impose a fine of 2.8 million RMB (approximately $431,088) against the company for violations of Chinese direct selling laws.

The SEC further alleged that a Nu Skin China employee reached out to the Party Official, who was an acquaintance, and requested that he propose a charity to receive a donation from Nu Skin China at the same time the AIC's investigation was ongoing. The Party Official allegedly proposed a charity, with which the Party Official was affiliated, that had not yet been established in the province. Senior personnel at Nu Skin China allegedly requested that the Party Official personally intervene in the AIC's investigation in exchange for the charitable donation to the Party Official's proposed charity.

According to the settlement documents, Nu Skin US, upon learning that Nu Skin China intended to make a donation, identified the potential FCPA risks and advised Nu Skin China to consult with a U.S. law firm based in China. The law firm allegedly included anti-corruption language in the proposed donation agreement prohibiting the use of the donation to influence government officials, but the language was subsequently removed from the final draft unbeknownst to Nu Skin US. However, the SEC's Order alleges that "Nu Skin US did not ensure that adequate due diligence was conducted by Nu Skin China with respect to charitable donations to identify links to government or political party officials and to prevent payments intended to improperly influence such persons in violation of the company's anticorruption policy and the FCPA."

In addition to the charitable donation, the Party Official allegedly requested that the company obtain college recommendation letters to U.S. universities from influential U.S. persons, which Nu Skin China labeled as a "top priority." According to the settlement documents, Nu Skin US subsequently reported that it had secured a prominent U.S. person to write a letter of recommendation for the Party Official's child.

According to the SEC's Order, two days after the donation ceremony, which was attended by the Party Official, the AIC notified Nu Skin China that it would not charge or fine the company in relation to violations of the direct selling laws.

Noteworthy Aspects

- Necessity of Performing Due Diligence on Charitable Contributions: Previous enforcement actions, such as the 2004 Schering-Plough case, have highlighted the use of charitable contributions to confer improper benefits to government officials in violation of the FCPA. While Nu Skin US attempted to address the FCPA risks posed by the charitable donation, the company failed to perform adequate due diligence on or monitor the contribution to ensure compliance safeguards were in place. Although the SEC's Order noted that Nu Skin US identified that the contribution posed some FCPA risk, Nu Skin US did not uncover the connection between the donation, the Party Official and the ongoing investigation, despite red flags. The SEC's Order also highlights the fact that, around the same time period, Nu Skin China requested that Nu Skin US engage an influential person to write college recommendation letters on behalf of the same Party Official, which suggests that the company should have investigated whether the charitable foundation had any connections to government officials, such as the Party Official. The SEC's Order emphasizes the need for companies to understand the purpose of charitable contributions and thoroughly vet whether any related government actions or officials may be influenced by such donations.

- Necessity of Ensuring that Compliance Safeguards Are In Place: The SEC's Order also notes that Nu Skin China engaged a U.S. law firm based in China to provide advice on risk mitigation and the law firm included anti-corruption provisions in the donation agreement. However, Nu Skin US did not monitor to ensure that the anti-corruption clauses were included in the final executed version of the contract, and the language was removed.

- Local Law Violation Cause of Alleged Bribery Scheme: The Nu Skin case demonstrates the importance of companies understanding the local law requirements in the countries where they operate. Nu Skin China allegedly failed to follow the local laws related to direct selling and as a result, faced an investigation by Chinese authorities. The case highlights the risks related to local law violations, which could lead to solicitations by local officials for improper benefits to cover up the violations or to have penalties dismissed.

Anheuser-Busch InBev Settles with SEC Over Improper Payments and Benefits Allegedly Provided to Officials in India and Violations of Whistleblower Protection Rules

On September 28, 2016, the SEC announced a settlement with AB InBev, a Belgium-based brewing company and issuer of securities on the New York Stock Exchange. Under the settlement, AB InBev agreed to pay approximately $6 million to the SEC for violations of the books-and-records and internal-accounting-controls provisions of the FCPA and the whistleblower protection provisions of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). The alleged violations involved AB InBev's now defunct joint venture with RJ Corp, InBev India International Private Limited (IIIPL).

From 2009 to 2012, AB InBev owned a 49 percent stake in IIIPL, which managed the marketing and distribution of beer for AB InBev's wholly-owned Indian subsidiary, Crown Beers India Private Limited (Crown). During this period, the SEC alleged that two third-party sales promoter companies hired by IIIPL made improper payments to Indian government officials to obtain beer orders and to extend the permissible daily brewing hours for Crown during several months in 2011. When IIIPL sought reimbursement from Crown for the promoters' activities, it inflated commissions and reimbursements to hide the improper payments. Crown, in turn, paid or accrued the expenses and recorded them in its books as legitimate promotional costs. Crown's books, including the illegitimate payments, were then consolidated into AB InBev's books.

In addition, the SEC identified multiple internal-accounting-controls failings of Crown. According to the SEC, Crown employees did not verify that contracts were executed with the promoter companies. Although AB InBev expedited an already planned internal audit of IIIPL upon receiving a compliance-related internal complaint in 2010, the audit failed to scrutinize the promoter company's activities or expenses. Moreover, the SEC Order noted that AB InBev did not address many of the issues identified in the 2010 audit until 2011 or early 2012.

Furthermore, the SEC alleged that in December 2012, AB InBev violated Dodd-Frank's whistleblower protection provisions when it entered into a separation agreement with a former Crown employee who had raised concerns about IIIPL's relationship with the third-party promoter companies on multiple occasions. After the employee was terminated in 2012, AB InBev and the employee entered into a separation agreement, which required the employee to "keep in strict secrecy and confidence" any "unique information ... that is not a matter of common knowledge or otherwise generally available to the public."

Following the execution of the agreement, the employee, who had previously communicated with the SEC, ceased to do so to avoid triggering the separation agreement's liquidated damages provision. It is unclear from the SEC's Order whether AB InBev knew that the employee had been cooperating with the Commission. Regardless, the SEC found that the language of AB InBev's separation agreement, which did not explicitly include an exception for reporting to authorities, "impeded the Crown Employee from communicating directly with the Commission staff." The SEC noted that AB InBev had executed similar agreements in the past.

According to the settlement, at the beginning of the investigation, AB InBev failed to cooperate fully. For example, it failed to report two separate compliance related complaints to the SEC, it took no immediate corrective steps when the SEC alerted it of allegations that IIIPL employees planned to destroy documents, it did not respond to subpoenas in a timely manner and it made broad assertions of privilege that stalled that investigation. However, the Order suggested that AB InBev's cooperation improved over time.

Noteworthy Aspects

- Continued Commitment to Protect Whistleblowers: This settlement marks the latest example of the SEC's continued commitment to aggressively enforce Dodd-Frank's whistleblower protection provisions, specifically with respect to companies' separation agreements. During the last quarter, Health Net, Inc. (which has since merged with Centene Corp) and BlueLinx Holdings Inc. also settled with the SEC in connection with such agreements. The newly appointed Chief of the SEC Whistleblower Office, Jane Norberg, stated, "[t]hreat of financial punishment for whistleblowing is unacceptable. We will continue to take a hard look at these types of provisions and fact patterns." In this case, the SEC noted that as part of its remediation efforts, AB InBev amended its separation agreements to include the following language: "I understand and acknowledge that notwithstanding any other provision in this Agreement, I am not prohibited or in any way restricted from reporting possible violations of law to a governmental agency or entity and I am not required to inform the Company if I make such reports."

- Application of Internal-Accounting-Controls Provisions to Affiliates: Under the FCPA's accounting provisions, an issuer that holds the majority voting power in an entity, including a joint venture, is strictly liable for the internal accounting controls of that entity. However, an issuer that holds "50 per centum or less of the voting power" must only proceed in good faith "to the extent reasonable under the issuer's circumstances" to cause the entity to establish and maintain a system of internal accounting controls. As noted, this matter involved two AB InBev affiliates. The first affiliate, Crown, is AB InBev's wholly-owned subsidiary. Therefore, AB InBev is strictly liable for failures in Crown's internal controls. Regarding the second affiliate, IIIPL, AB InBev owned a minority stake and, significantly, had less than 50 percent of the voting power due to the fact that AB InBev's joint venture partner had the right to appoint the chairman who held the tiebreaking vote. Thus, it appears that a good faith standard applied. Ultimately, the SEC findings only alleged internal-accounting-control failings with respect to the activities of Crown, which reimbursed IIIPL for the alleged illicit transactions with the promoter companies. It did not allege any violations with respect to IIIPL's failures.