Proposed Regulations Provide Guidance on FDII and GILTI Deductions

Tax Alert

On March 4, 2019, Treasury and the IRS issued proposed regulations (Proposed Regulations) under section 250.1 The 2017 Tax Cuts and Jobs Act added section 250, which provides a deduction for a domestic corporation's foreign derived intangible income (FDII) and global intangible low-taxed income (GILTI). The deduction, intended to "neutralize the role that tax considerations play when a domestic corporation chooses the location of intangible income attributable to foreign market activity,"2 reduces the effective tax rate on income domestic companies earn from foreign sales and services.3 This reduced effective rate is achieved through a deduction equal to the sum of (1) 37.5 percent of the domestic corporation's FDII, plus (2) 50 percent of the domestic corporation's (a) GILTI and (b) dividends received under section 78 attributable to GILTI.4

The Proposed Regulations address issues associated with calculating a taxpayer's section 250 deduction – including how to compute FDII and its components – as well as rules applicable to partnerships, tax-exempt corporations, individuals, and consolidated groups. For corporations, the Proposed Regulations clarify that the section 250 deduction is determined at the consolidated group level; items are aggregated to compute an overall deduction, which is allocated to members based on each member's contribution to foreign derived deduction eligible income (FDDEI) and GILTI. The Proposed Regulations categorize transactions – particularly the provision of services – and apply different rules to determine whether transactions in each category generate FDDEI. Taxpayers should evaluate how their transaction flows align with these categories and consider whether alternatives would produce a more favorable result. To the extent the categories in the Proposed Regulations do not reach reasonable results for a particular business or industry, taxpayers should consider engaging in the notice-and-comment process. Written comments to the Proposed Regulations are due May 6, 2019.

Statutory Overview

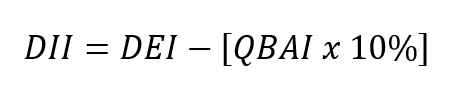

To determine its section 250 deduction, a domestic corporation must first determine its FDII amount. This determination is made through a multistep process in which the corporation must calculate (1) deduction eligible income (DEI), (2) FDDEI, (3) qualified business asset investment (QBAI), and (4) deemed intangible income (DII).

DEI is defined as gross income (reduced by deductions allocable to such income, including taxes), but not including: (1) income under Subpart F, (2) GILTI, (3) financial services income, (4) dividends received from controlled foreign corporations (CFCs), (5) domestic oil and gas extraction income, and (6) foreign branch income.5 Next, the corporation must determine FDDEI, the amount of DEI which is attributable to (1) the sale of property to any foreign person for a foreign use or (2) services provided to any person not located within the United States or with respect to property that is not located in the United States.6 Then, the corporation must determine its QBAI, which is the average of the adjusted bases in depreciable tangible property used in the corporation's trade or business (specified tangible property) to generate DEI.7 Finally, the corporation must calculate DII, which is DEI less the deemed tangible income return (DTIR).8 A corporation's DTIR is 10 percent of its QBAI.9 The amount of DII can be represented as follows:

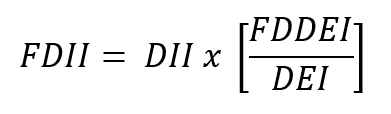

The corporation can then calculate its FDII and corresponding deduction. FDII is determined by multiplying the corporation's DII by the foreign-derived ratio (i.e., the ratio of FDDEI to DEI), represented as follows:10

The FDII deduction is 37.5 percent of the corporation's FDII. However, the amount of the deduction is subject to a taxable income limitation.11 If the sum of the corporation's FDII and GILTI amount exceeds the corporation's taxable income for the taxable year (determined without regard to section 250), the excess is allocated pro rata to reduce the corporation's FDII and GILTI for purposes of the section 250 deduction.12 The amount by which FDII must be reduced is as follows:

The corporation then calculates the amount of the FDII deduction based on the reduced FDII amount.

Overview of Proposed Regulations

The Proposed Regulations address issues associated with calculating a taxpayer's section 250 deduction – including how to compute FDII and its components, QBAI, DEI, and FDDEI – as well as ordering rules that take into account other limitations on deductions that can impact the limitation of the amount of DEI subject to the FDII calculation, and rules applicable to partnerships, tax-exempt corporations, individuals, and consolidated groups. While the section 250 deduction is only available to domestic entities taxed as C corporations, the Proposed Regulations provide that the 50 percent section 250 deduction for GILTI (but not FDII) is available to U.S. individuals shareholders of CFCs if they make a section 962 election.13

Computing the Section 250 Deduction

The section 250 deduction is subject to a taxable income limitation, taking into account applicable deductions (other than the section 250 deduction).14 The Proposed Regulations provide ordering rules that govern how taxpayers should apply other limitations on deductions, i.e., the business interest limitation of section 163(j) and the limitation of the net operating loss deduction under 172(a)(2), in coordination with section 250.

First, the domestic corporation must compute the tentative amount of FDII and the tentative amount of section 250 deduction (Tentative Section 250 Deduction), taking into account all deductions, but without regard to sections 163(j), 172(a), or 250(a)(2).15 Second, the corporation must compute the amount of business interest allowed after the application of section 163(j) (Business Interest), taking into account the Tentative Section 250 Deduction but without regard to section 172(a).16 Third, the corporation computes the amount of net operating loss deduction under section 172(a) (NOL Deduction), taking into account its Business Interest and the taxable income limitation of section 172(a)(2), but without regard to the amount of the section 250 deduction (including the Tentative Section 250 Deduction).17 Fourth, the corporation computes the amount of FDII, taking into account both its Business Interest and its NOL Deduction.18 Finally, the corporation can determine the section 250 deduction, taking into account the section 250(a)(2) limitation and its Business Interest and NOL Deduction.19 The interaction of these steps is shown in the chart below:

| CALCULATION | ITEMS CONSIDERED | ITEMS NOT CONSIDERED |

| Step One: Tentative Section 250 Deduction |

All other deductions |

Business Interest |

| Step Two: Business Interest |

Tentative Section 250 Deduction | NOL Deduction |

| Step Three: NOL Deduction |

Business Interest Taxable Income Limitation of Section 172(a)(2) |

Section 250 Deduction Tentative Section 250 Deduction |

| Step Four: FDII |

Business Interest NOL Deduction |

N/A |

| Step Five: Section 250 Deduction |

Business Interest NOL Deduction Section 250(a)(2) |

N/A |

Treasury and the IRS request comments on the ordering rule.20

DEI and FDDEI

The Proposed Regulations provide guidance as to the determination of DEI and FDDEI. Generally, a corporation must determine "gross DEI" and "gross FDDEI" and allocate and apportion expenses to arrive at DEI and FDDEI.21 As noted above, DEI excludes certain types of income, including foreign branch income. The Proposed Regulations generally define foreign branch income by reference to the definition in the proposed foreign tax credit (FTC) regulations.22 However, for purposes of FDII, income from the sale of a branch asset (including, e.g., the sale of an interest in a disregarded entity or partnership) is considered foreign branch income and is therefore excluded from FDDEI, even though it may not be considered foreign branch income for purposes of the foreign tax credit limitation.23 The proposed FTC regulations include rules to recharacterize transfers of intangible property of a type described in section 367(d)(4) between a foreign branch owner and a foreign branch. To the extent that taxpayers are negatively impacted by the extension of these recharacterization rules to the FDII context, these Proposed Regulations present another opportunity to comment.

The Proposed Regulations apply section 861 expense apportionment rules to determine DEI and FDDEI.24 For purposes of apportioning expenses to DEI and FDDEI, the section 250 deduction is not treated as giving rise to exempt income or assets.25 Furthermore, research and experimental expenditures are allocated and apportioned without taking into account the exclusive apportionment rule of Treas. Reg. § 1.861-17(b), which apportions expense based on the location of research and experimental activity. The Proposed Regulations state that the foreign-derived ratio cannot exceed 1, for example in the event that losses attributable to U.S. sales cause FDDEI to exceed total DEI.26

The Proposed Regulations also apply an aggregate approach to partnerships with domestic corporate partners.27 As a result, a domestic corporation that is a partner in a partnership determines its section 250 deduction by taking into account its distributive share of a partnership's gross DEI, gross FDDEI, and deductions, and its share of the partnership's specified tangible property.

QBAI

The Proposed Regulations generally determine QBAI in the same manner as QBAI is determined for purposes of the GILTI rules of section 951A.28 The Proposed Regulations also include anti-avoidance rules for certain transfers of tangible property entered into with a principal purpose of decreasing the amount of DTIR. Where applicable, these rules treat the transferor as if it owned the transferred property solely for purposes of determining QBAI. With respect to related party transfers, the rule applies generally to transfers of tangible property to related parties if the taxpayer (or a FDII-eligible affiliate) leases the same or substantially similar property from a related party within a two-year period around the transfer; moreover, a principal purpose of decreasing DTIR is deemed if the lease occurs with six months of the transfer.29 With respect to unrelated party transactions, the anti-avoidance rule applies if either (1) the reduction in the domestic corporation's DTIR is a "material factor in the pricing of the arrangement," or (2) the reduction in the domestic corporation's DTIR is a "principal purpose of the arrangement" based on all facts and circumstances.30

Gross FDDEI

For the purposes of calculating a domestic corporation's foreign-derived ratio, FDDEI is gross FDDEI less its allocable deductions.31 Gross FDDEI is defined in the Proposed Regulations as the portion of a corporation's gross DEI that is derived from its FDDEI sales and services.32 Section 250 provides different rules for sales and services.33 Transactions consisting of both sales and services are classified based on the "predominant character" of the transaction.34 The Proposed Regulations do not address the extent to which a domestic corporation can disaggregate a transaction into an independent sale and service. The Proposed Regulations provide specific rules for the documentation of foreign status or foreign use, including rules for determining whether the seller or service provider had "reason to know" that the transaction is not for foreign use.35

1. Gross FDDEI from Sales of Property

For a sale to qualify as a FDDEI sale, section 250(b)(4)(A) requires the sale to be to a foreign person for foreign use.36 The Proposed Regulations provide guidance as to the meaning of "foreign person" for this purpose. Significantly, the Proposed Regulations treat a partnership as a person such that a sale to a foreign partnership is a sale to a foreign person, and sale to a domestic partnership is not a sale to a foreign person.37 Treasury and the IRS request comments on whether an aggregate approach for partnerships would be more effective in some circumstances.38 The Proposed Regulations also contain a favorable clarification regarding foreign military sales, providing that a sale to the U.S. government for the benefit of a foreign government under the Arms Export Control Act of 1976 is treated as a sale to a foreign person.39 Treasury and the IRS request comments on how a taxpayer can demonstrate that a particular sale was made pursuant to the Arms Export Control Act.40

The analysis of whether a sale of property is for foreign use depends on whether there is a sale of general property (General Property) or intangible property (IP).41 General Property is property other than IP, securities, or financial contracts in commodities.42 IP has the same meaning given to it in section 367(d)(4).43

General Property is considered sold for foreign use if either (1) there is no domestic use of the property within three years of delivery or (2) the property is subject to additional manufacture, assembly, or other processing outside the United States before there is domestic use of the property.44 General Property is subject to manufacture, assembly, or processing if, based on facts and circumstances, there is either (1) a physical and material change to the property (not including minor assembly, packaging, or labeling) or (2) the property is incorporated as a component into a second product.45 Property is considered incorporated as a component only if the property's fair market value constitutes no more than 20 percent of the fair market value of the subsequent product.46 The domestic corporation must obtain documentation to establish that General Property is for foreign use, such as (1) a written statement from the recipient that the property is for a foreign use, (2) a binding contract which provides that the property is for a foreign use by the recipient, or (3) proof of shipment to a foreign address.47 The Preamble requests comments on how these rules will affect supply chains.48

IP is considered sold for foreign use based on revenue earned from exploiting the IP outside of the United States (i.e., the location of end-user customers).49 The rule for additional manufacturing that applies to General Property does not apply to IP because Treasury believes that IP is not "subject to" manufacture.50 However, Treasury and the IRS request comments on whether an analogous manufacturing rule for IP is appropriate.51

2. Gross FDDEI from Services

The Proposed Regulations create four exclusive and non-overlapping categories of FDDEI services: (1) proximate services, (2) property services, (3) transportation services, and (4) general services. Each service transaction must first be classified into one of these categories.52 The Proposed Regulations provide different rules to determine whether, in each case, a service is provided to a person or with respect to property outside of the United States.

Proximate services, such as on-site consulting, are services performed in the physical presence of the service recipient.53 A proximate service is a FDDEI service if it takes place outside of the United States, and may be a FDDEI service in part if it takes place in part outside of the United States.54 Note that a service provided by a domestic corporation through a foreign branch cannot be a FDDEI service.

Property services, such as assembly or repair, are services provided to tangible property at the location of the property.55 A property service is a FDDEI service if the property is located outside of the United States.56 Treasury and the IRS request comments as to the treatment of property sent to the United States temporarily for maintenance or repair.57 Again, a service provided by a domestic corporation through a foreign branch cannot be a FDDEI service.

Transportation services are services to transport a person or property using any mode of transportation.58 The Proposed Regulations provide that a transportation service is a FDDEI service based on the origin and destination of the transported person or property.59 If both the origin and destination are outside of the United States, 100 percent of the gross income will be included in gross FDDEI.60 If either the origin or the destination is outside of the United States, 50 percent of the gross income from the service will be included in gross FDDEI.61

Finally, the category of "general services" acts as a residual category for previously uncategorized services.62 Whether such a service is a FDDEI service depends on the character and location of the recipient – for business recipients, the location is based on the location of operations of the recipient and any related parties that receive a benefit, within the meaning of Treas. Reg. § 1.482-9(l)(3), from the service.63 For consumer recipients, the location is based on where the consumer resides when the service is provided.64

3. Gross FDDEI for Related Party Transactions

Section 250 imposes additional requirements on related party transactions, and there are different standards based on whether the transaction is a sale or a service.65 For a resale of purchased property by a related party, the Proposed Regulations require the domestic corporation to document that the related party will sell the property to an unrelated party for an ultimate foreign use.66 Further, the unrelated party sale must occur on or before the FDII filing date, defined as the date, including extensions, of the seller's tax return for the year of related party sale.67 However, if the unrelated party sale happens after the taxpayer files its return for the year of the related party sale, then the taxpayer must file an amended return to include the income from the related party sale in FDDEI.68 These administrative requirements may be burdensome for taxpayers, and the Preamble requests comments on whether alternatives should be considered in lieu of requiring an amended return.69 If the related party will use the purchased property in manufacturing or in the provision of services, the sale is treated as a FDDEI transaction if the seller reasonably expects that greater than 80 percent of the revenue of the foreign related party will be from unrelated party transactions that are FDDEI transactions.70

In the case of related party services, section 250(b)(5)(C)(ii) provides that a service provided to a related party does not produce FDDEI unless the service is "not substantially similar" to services provided by the related person to persons in the United States. The Proposed Regulations limit this "round tripping" rule to General Services provided to business recipients.71 The Proposed Regulations introduce two tests – the "benefit test" and the "price test" – to determine whether a related party service is substantially similar to a service provided by the related party to U.S. customers.72 The service is not a FDDEI service under the benefit test if 60 percent or more of the benefits conferred by the related party service are to persons located within the United States.73 The service is not a FDDEI service under the price test if 60 percent or more of the price that domestic recipients pay to the related party is attributable to the domestic corporation's service to the related party.74

Effective Date

The rules in the Proposed Regulations generally apply to any domestic corporation's taxable year that ends after March 4, 2019.75 The preamble states that taxpayers may rely on the Proposed Regulations for taxable years ending before March 4, 2019, i.e., 2018 in the case of calendar year taxpayers.76

For further information, please contact:

Layla J. Asali, lasali@milchev.com, 202-626-5866

Rocco V. Femia, rfemia@milchev.com, 202-626-5823

Jennifer E. Maul*

Loren C. Ponds*

*Former Miller & Chevalier attorney

---------

1REG-104464-18 (Mar. 4, 2019). The Proposed Regulations were published in the Federal Register on March 6, 2019. 84 F.R. 8188. All "section" references are to the Internal Revenue Code of 1986, as amended and currently in effect.

284 F.R. at 8189.

3Section 250(a)(1). Assuming the taxable income limitation of section 250(a)(2) does not apply, the effective rate of tax on "intangible" income from foreign sales and services is 13.125 percent in taxable years beginning before January 1, 2025, and 16.406 percent thereafter (assuming a 21 percent corporate income tax rate). Section 250(a)(3).

4Section 250(a)(1).

5Section 250(b)(3).

6Section 250(b)(4).

7Section 951A(d).

8Section 250(b)(2)(B).

9Section 250(b)(2).

10Section 250(b)(1).

11Section 250(a)(2).

12Id.

13Prop. Treas. Reg. § 1.962-1(b).

14Section 250(a)(2).

1584 F.R. at 8190; see Prop. Treas. Reg. § 1.250(a)-1(f), ex. 2.

16Id.; see section 163(j)(8)(A)(iii); Prop. Treas. Reg. §§ 1.163(j)-1(b)(1)(i)(B), (b)(37)(ii).

1784 F.R. at 8190; see Prop. Treas. Reg. § 1.250(a)-1(f), ex. 2; see also section 172(d)(9).

18Prop. Treas. Reg. § 1.250(a)-1(c)(4).

1984 F.R. at 8190; see Prop. Treas. Reg. § 1.250(a)-1(f), ex. 2.

2084 F.R. at 8190.

21See Prop. Treas. Reg. §§ 1.250(b)-1(c)(14), 1.250(b)-1(c)(15), 1.250(b)-1(d).

22Prop. Treas. Reg. § 1.904-4(f).

23Prop. Treas. Reg. § 1.250(b)-1(c)(11).

24Prop. Treas. Reg. § 1.250(b)-1(d)(2).

25Prop. Treas. Reg. § 1.861-8(d)(2)(ii)(C)(4).

26Prop. Treas. Reg. § 1.250(b)-1(c)(13).

27Prop. Treas. Reg. § 1.250(b)-1(e)(1).

28Compare Prop. Treas. Reg. § 1.951A-3 with Prop. Treas. Reg. § 1.250(b)-2.

29Prop. Treas. Reg. § 1.250(b)-2(h)(1) and (3).

30Prop. Treas. Reg. § 1.250(b)-2(h)(2).

31Prop. Treas. Reg. § 1.250(b)-1(c)(12).

32Prop. Treas. Reg. § 1.250(b)-1(c)(15).

33Section 250(b)(4).

34Prop. Treas. Reg. § 1.250(b)-3(e).

35See, e.g., Prop. Treas. Reg. § 1.250(b)-4(c).

36Prop. Treas. Reg. § 1.250(b)-4(b).

37Prop. Treas. Reg. § 1.250(b)-3(g).

3884 F.R. at 8192.

39Prop. Treas. Reg. § 1.250(b)-3(c).

4084 F.R. at 8193.

41See Prop. Treas. Reg. §§ 1.250(b)-4(d), (e).

42Prop. Treas. Reg. § 1.250(b)-3(b)(3).

43Prop. Treas. Reg. § 1.250(b)-3(b)(4).

44Prop. Treas. Reg. § 1.250(b)-4(d)(2)(i).

45See Prop. Treas. Reg. § 1.250(b)-4(d)(2)(iii).

46Prop. Treas. Reg. § 1.250(b)-4(d)(2)(iii)(C).

47Prop. Treas. Reg. § 1.250(b)-4(d)(3).

4884 F.R. at 8194.

49Prop. Treas. Reg. § 1.250(b)-4(e)(1).

5084 F.R. at 8195.

51Id.

52See Prop. Treas. Reg. §§ 1.250(b)-5(b), (c)(4)-(7).

53Prop. Treas. Reg. § 1.250(b)-5(c)(6). The service provider must be in the physical presence of the recipient more than 80 percent of the time. Id.

54Prop. Treas. Reg. § 1.250(b)-5(f).

55Prop. Treas. Reg. § 1.250(b)-5(c)(5). The service provider must perform the service at or near the location of the tangible property more than 80 percent of the time. Id.

56Prop. Treas. Reg. § 1.250(b)-5(g).

5784 F.R. at 8197.

58Prop. Treas. Reg. § 1.250(b)-5(c)(7).

59Id.

60Id.

61Prop. Treas. Reg. § 1.250(b)-5(h).

62Prop. Treas. Reg. § 1.250(b)-5(c)(4).

63Prop. Treas. Reg. §§ 1.250(b)-5(e)(2), (4).

64Prop. Treas. Reg. § 1.250(b)-5(d)(2).

65See section 250(b)(5)(C).

66Prop. Treas. Reg. § 1.250(b)-6(c)(1).

67Prop. Treas. Reg. § 1.250(b)-6(c)(1)(i).

68Id.

6984 F.R. at 8198.

70Prop. Treas. Reg. § 1.250(b)-6(c)(1)(ii).

71Prop. Treas. Reg. § 1.250(b)-6(d)(1).

72Prop. Treas. Reg. § 1.250(b)-6(d)(2).

73Prop. Treas. Reg. § 1.250(b)-6(d)(2)(i).

74Prop. Treas. Reg. § 1.250(b)-6(d)(2)(ii).

75Prop. Treas. Reg. § 1.250-1(b).

7684 F.R. at 8201, as corrected by 84 F.R. 14901. The unofficial publication of the Proposed Regulations provided that both the applicability and reliance dates would reference the date the Proposed Regulations were filed in the Federal Register, i.e., March 4, 2019.

The information contained in this communication is not intended as legal advice or as an opinion on specific facts. This information is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. For more information, please contact one of the senders or your existing Miller & Chevalier lawyer contact. The invitation to contact the firm and its lawyers is not to be construed as a solicitation for legal work. Any new lawyer-client relationship will be confirmed in writing.

This, and related communications, are protected by copyright laws and treaties. You may make a single copy for personal use. You may make copies for others, but not for commercial purposes. If you give a copy to anyone else, it must be in its original, unmodified form, and must include all attributions of authorship, copyright notices, and republication notices. Except as described above, it is unlawful to copy, republish, redistribute, and/or alter this presentation without prior written consent of the copyright holder.